The Future Arrives for Five Clean Energy

Technologies – 2016 Update

September 2016

Revolution…Now

Contributors i

Acknowledgments

Primary Author

U.S. Department of Energy

Paul Donohoo-Vallett, DOE Ofce of Energy Efciency & Renewable Energy

Contributing Authors

U.S. Department of Energy

Patrick Gilman, DOE Wind Energy Technologies Ofce

David Feldman, National Renewable Energy Laboratory

James Brodrick, DOE Building Technologies Ofce

David Gohlke, DOE Vehicle Technologies Ofce

Roland Gravel, DOE Vehicle Technologies Ofce

Amy Jiron, DOE Building Technologies Ofce

Carol Schutte, DOE Vehicle Technologies Ofce

Sunita Satyapal, DOE Fuel Cell Technologies Ofce

Tien Nguyen, DOE Fuel Cell Technologies Ofce

Paul Scheihing, DOE Advanced Manufacturing Ofce

Blake Marshall, DOE Advanced Manufacturing Ofce

Sarah Harman, DOE Ofce of Energy Efciency & Renewable Energy

Notice

This report is being disseminated by the U.S. Department of Energy (DOE). As such, this document was prepared

in compliance with Section 515 of the Treasury and General Government Appropriations Act for Fiscal Year 2001

(Public Law 106-554) and information quality guidelines issued by DOE.

Reference herein to any specic commercial product, process, or service by trade name, trademark, manufacturer,

or otherwise does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United

States government or any agency thereof.

Table of Contents iii

Table of Contents

Accelerating Progress . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Wind . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Solar PV: Utility-Scale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Solar PV: Distributed. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

LEDs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Electric Vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Revolution Next. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Super Trucks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Smart Buildings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Lightweighting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Stacked for Success: Fuel Cells . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

ISO 50001 and the Superior Energy Performance Program in the Manufacturing Sector . . . . . . . . . . . . . . 15

Supercharging the Grid with Batteries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Big Area Additive Manufacturing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

LAND-BASED WIND

Wind accounted for

41%

of all new generation capacity installed in the US in 2015

EVS

Over

490,000 EVs have

been sold through August of 2016

DISTRIBUTED SOLAR PV

The

millionth distributed photovoltaic

system was installed early in 2016

UTILITY-SCALE SOLAR PV

Revolution...Now

Accelerating Clean Energy Deployment

LEDS

Total A-Type LED bulb

installations surpassed

200 million

in 2015, more than

doubling since the

previous year

In 2015 total capacity grew

43% over 2014, reaching

nearly 14,000 MW

Accelerating Progress 1

Accelerating Progress

Decades of investments by the federal government and industry in ve key clean energy technologies are making

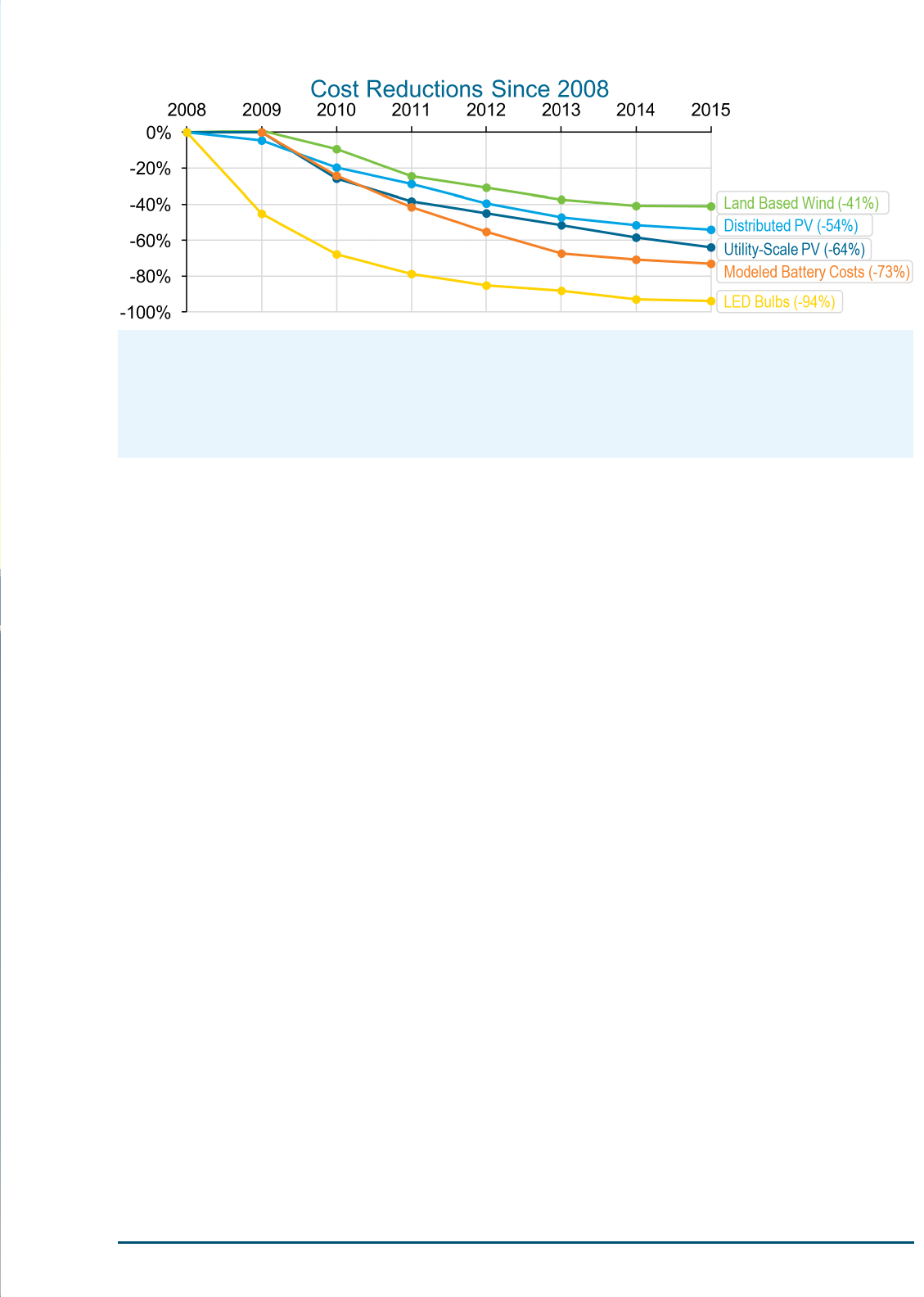

an impact today. The cost of land-based wind power, utility and distributed photovoltaic (PV) solar power, light

emitting diodes (LEDs), and electric vehicles (EVs) has fallen by 41% to as high as 94% since 2008. These cost

reductions have enabled widespread adoption of these technologies with deployment increasing across the board.

Combined, wind, utility-scale and distributed PV accounted for over 66% of all new capacity installed in the nation

in 2015. [6] Total installations of LED bulbs have more than doubled from last year, [5] and cumulative EV sales

are about to pass the half-million mark. [7]

These technologies are now readily available and our country has already begun to reap the benets through their

increased adoption. As these clean technologies are broadly deployed there is a reduction in the emissions that

contribute to climate change, the air we breathe is better quality because of a decline in air pollutants, and we are

expanding economic opportunities for American workers and manufacturers. In 2014 the manufacturing sectors for

wind turbines, photovoltaic panels, lithium ion batteries, and LEDs have added $3.8 billion dollars in value to the

U.S. economy. [8]

As we continue to advance international action on climate change under the Paris Agreement – which established a

long-term worldwide framework to reduce global greenhouse gas emissions – these ve technologies have and will

play a critical role in providing opportunities to reach global climate goals.

The technologies highlighted in this report exemplify how the clean energy revolution is already underway, is

already providing real-world benets, and continues to promise new solutions on the horizon to address our most

pressing energy challenges.

Through the Mission Innovation initiative announced in 2015, 20 countries and the European Union have

committed to double their respective clean energy research and development investment over ve years. This surge

will surely lead to breakthroughs in other clean energy technologies that today still seem futuristic, just as many of

the technologies in this report seemed just a few years ago.

We have seen incredible achievements from these technologies, but we must continue to strive to innovate and

develop the technologies that remain to be unlocked.

In addition to the emerging technologies highlighted in last year's report — super efcient trucks, smart buildings,

and light weighting materials — this report will highlight four additional technologies — hydrogen fuel cells, smart

energy management, grid connected batteries, and big area additive manufacturing — which are on the cusp of

future widespread deployment.

LAND-BASED WIND

Wind accounted for

41%

of all new generation capacity installed in the US in 2015

EVS

Over

490,000 EVs have

been sold through August of 2016

DISTRIBUTED SOLAR PV

The

millionth distributed photovoltaic

system was installed early in 2016

UTILITY-SCALE SOLAR PV

Revolution...Now

Accelerating Clean Energy Deployment

LEDS

Total A-Type LED bulb

installations surpassed

200 million

in 2015, more than

doubling since the

previous year

In 2015 total capacity grew

43% over 2014, reaching

nearly 14,000 MW

Notes: Land based wind costs derived from levelized cost of energy from representative wind sites from references [1]

and [2]. Distributed PV is average residential installed cost from reference [3]. Utility-Scale PV is median installed cost

for utility-scale PV systems from reference [4]. Modeled battery costs are at high-volume production of battery systems,

derived from DOE/UIS Advanced Battery Consortium PHEV Battery development projects. LED bulbs are for A-type

bulbs from reference [5].

REVOLUTION...NOW

2 Wind

Wind

Blowing Down Barriers

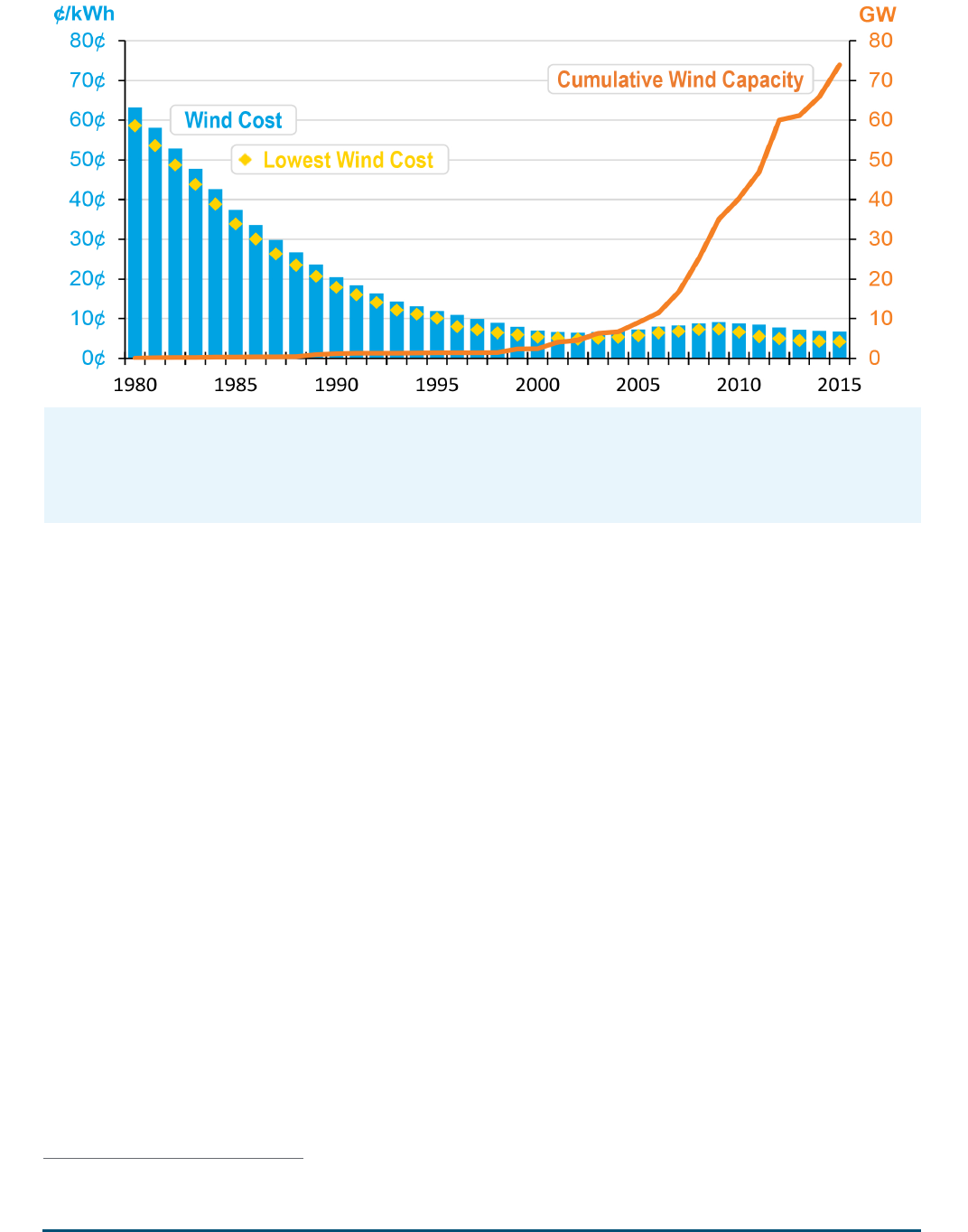

Wind power surged in 2015 with capacity growing by 12% since 2014, representing 41% of all new capacity

installed in the U.S. last year. [9] As of 2015, there were nearly 74,000 megawatts (MW) of utility-scale wind

power deployed across 41 states and territories [9]—enough to generate electricity for more than 17 million

households.

Overall, wind capacity has nearly tripled since 2008. Wind provided nearly 5% of total U.S. electricity generation

in 2015. In 23 states more than 500 MW of wind have been installed, and twelve states have seen their wind

generation exceed 10% of total in-state electricity generation. [9] This intense ramp up in installed generation has

yielded enormous benets. In 2015, wind power in the U.S. reduced annual carbon dioxide emissions by more than

132 million metric tons and decreased water consumption by more than 73 billion gallons.

These environmental benets are in addition to the nearly 90,000 U.S. manufacturing, construction, and wind

operations jobs contributing to a stronger U.S. economy. [10] In whole, the domestic manufacturing of wind

turbine components was able to add approximately $2 billion to the U.S. economy in 2014 alone. [8]

Wind in the Sales

This success of wind deployment has been enabled, in part, by recent cost reductions of wind power as U.S. wind

prices have reached all-time lows. Power purchase agreements for wind have fallen from rates of up to 7 cents/

kilowatt-hour (kWh) in 2009 to an average of 2 cents/kWh today in certain regions of the country.

This signicant reduction in cost and massive increase in deployment in a few years is a result of multiple

factors, including government investments, infrastructure development, and federal and state incentives. First,

DOE invested $2.4 billion dollars in wind research and development between 1976 and 2014. These continued

investments in key technology improvements such as the taller turbines and longer blades highlighted below have

helped drive down cost and improve performance.

Cost data from references are inflation adjusted to dollar year 2015, and exclude the production tax credit. “Wind Cost” data

estimates the levelized cost of energy from a representative wind site from references [1] and [2] and “Lowest Wind Cost”

represents costs derived from power purchase agreements from good to excellent wind resource sites in the interior of the

country as reported in reference [9]. Deployment data also from reference [9]. 1 gigawatt (GW) = 1,000 megawatts (MW).

1 One large capacity project was excluded from reference [9] based on unusual circumstances identied in the citation.

2 Wind generated 190,927 GWh in 2015. [18] The average American household consumed 10,932 kWh in 2014. [96]

3 Note that these prices come from reference [9] and include the effect of the federal PTC and as such are lower than what is displayed in the chart above.

4 Ination adjusted to 2015 dollars using U.S. Bureau of Economic Analysis GDP budget deator. Investment data and impacts for 1978-2008 from reference [97], data for 2009-2014 investments from reference [98].

Wind 3

Additionally new transmission expansion projects, such as the recently completed Texas Competitive Renewable

Energy Zone transmission build-out, have enabled wind development in more areas of the country — such as the

central part of the country that already has optimal wind resource locations. Expanded coordination among grid

operators has also increased the ability of the grid to accept higher levels of wind generation. [9]

Finally, policy has played a vital role in driving continued deployment of wind at both the state and national level.

State renewable portfolio standards have created mandates to build renewable energy in more than half the states

in the country. At the federal level, the production tax credit (PTC) has provided a nancial incentive to wind

projects, increasing their value relative to other generation technologies.

Together, these investments, infrastructure projects, and policies have made wind a low-cost, zero-carbon

alternative that contributes to the transformation of the U.S. electricity generation portfolio.

New Windows of Opportunity

Continued innovation in next generation wind technologies could soon enable cost-competitive wind in new areas

and new markets.

Beyond lowering costs in existing markets around the country, taller towers and longer blades could allow for

development of more wind projects in areas like the Southeastern U.S. that historically have not seen signicant

wind development. For example, a wind turbine installed today on average has 108% longer blades and is 48%

taller than one installed in 1999. [9] The longer blades allow each turbine to capture more energy, and taller towers

allow access to the stronger and more consistent wind speeds that occur at higher altitudes in many parts of the

country. Combined, these innovations allow each turbine to produce more electricity, reducing both the number of

turbines needed to produce a given amount of electricity and the land area needed for their installation.

These innovations enable a new generation of more cost-effective wind power. DOE estimates that the continued

development of taller wind towers coupled with larger rotors and advanced turbine designs would allow wind to be

cost-effectively deployed across the country. [11]

In addition, the development of wind energy in the waters off our nation’s coasts holds enormous potential. The

technical potential of offshore wind resources is enough to generate more electricity than twice what the U.S.

generated from all sources of electricity in 2015. [12]

The nation will have begun to take advantage of this offshore wind potential later this year as the 30 MW Block

Island project, located off the shore of Rhode Island, should be fully operational by the end of 2016. This will be

the rst commercial offshore wind power plant to operate in the U.S. By the end of 2015, the Department of the

Interior had awarded 11 commercial leases totaling 14,600 MW of capacity. [12] While the domestic offshore wind

industry still faces challenges, the potential of this technology to capture high wind resources close to coastal load

centers makes it a key future source of clean electricity for the nation.

Wind is also being purchased by new types of customers beyond traditional utilities. In 2015 nearly 2,000 MW

of wind power was contracted by corporations, representing companies across the retail, nancial, technology,

and manufacturing sectors — rapid growth considering only about 100 MW of wind power was contracted by

corporations in 2011. [13] This investment has been driven by a combination of competitive prices, environmental

responsibility, and the desire to invest in local economies.

Whirlwind of Activity

At the end of 2015, more than 110,000 MW of wind power was being considered by utilities and transmission

system operators for installation across the country representing nearly a third of all new proposed electricity

generation capacity. [9] Wind has massive untapped potential, as shown in a recent DOE report, Wind Vision, which

outlined how wind could generate 20% of the nation’s electricity by 2030 and 35% by 2050. [14] Technological

advancements are expected to continue to drive down costs in the future — a recent elicitation of wind experts

indicated wind energy costs could fall another 35% by 2050. [15]

With continuous technological innovation, transmission expansion, and continued federal and state support, wind

can continue to grow and unlock its wide array of benets in all 50 states.

REVOLUTION...NOW

4 Solar PV: Utility-Scale

Solar PV: Utility-Scale

Shedding Light on Expanded Solar Deployment

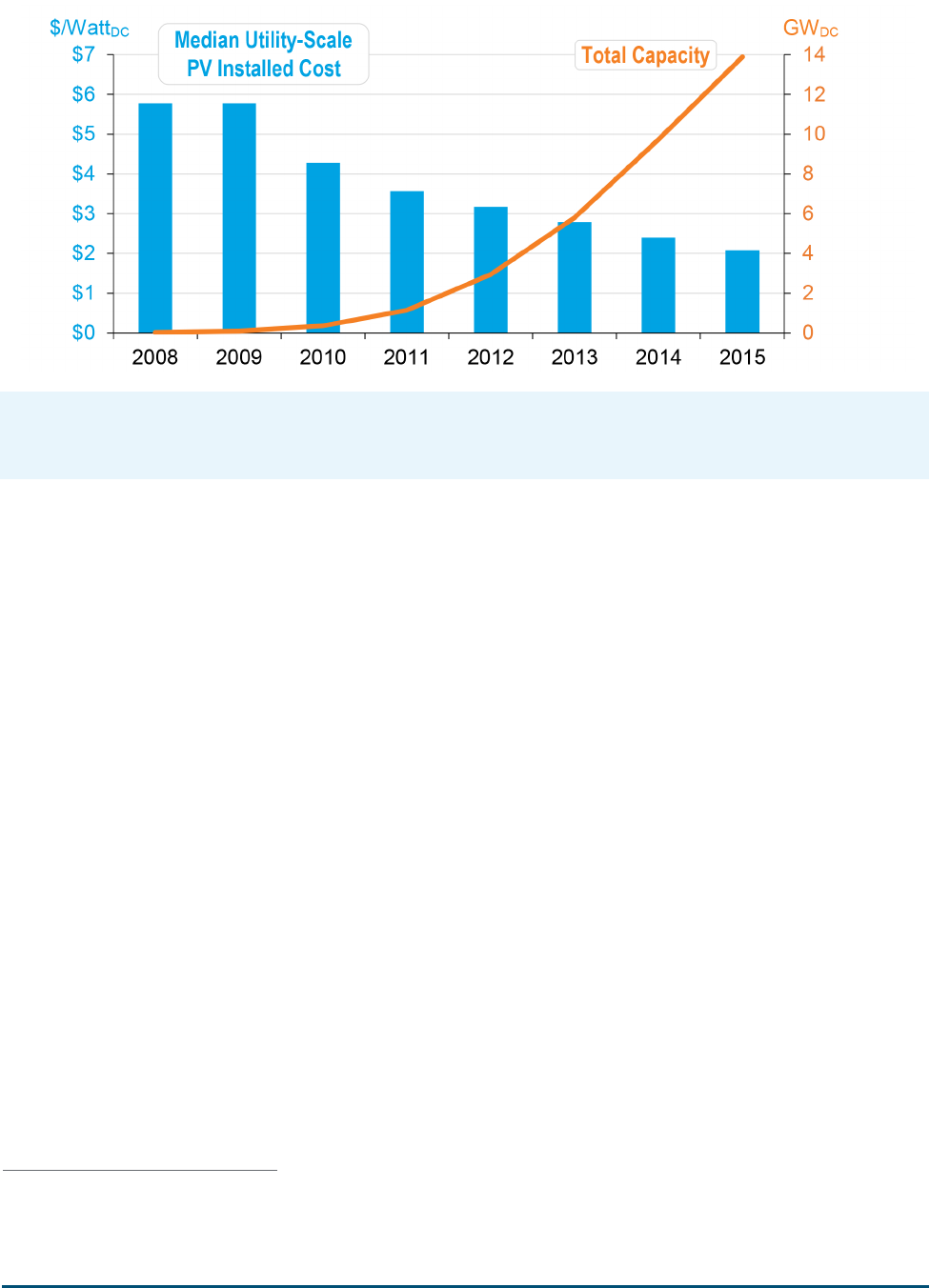

Annually, enough solar energy and land area is available in this country for utility-scale solar PV to generate ten

times the energy needed to power the entire nation. The challenge really lies in cost-effectively capturing and

converting this sunlight into useful forms of energy. However, signicant cost reductions in recent years has led

to expanded deployment of utility-scale PV, and nationally we are poised to take advantage of this nearly limitless

source of energy.

Utilities and the power sector are installing more utility-scale PV, as the installation cost of utility-scale PV has

steadily declined year after year, falling over 64% since 2008. This drop in cost has enabled explosive growth with

total capacity reaching more than 13,900 Megawatts (MW) in 2015, a growth of 43% over 2014. [16] The amount

of capacity installed in 2015 represented 15% of all utility-scale domestic electric generation capacity installed that

year. [6] This deployment trend continues to accelerate. In 2015, utility-scale PV generated 23 billion kWh, [17]

enough electricity to power over 2.1 million American homes. In the rst half of 2016, utility-scale PV generated

15 billion kWh – a 34% increase over the same time period as last year. [18]

The Dawn of New Markets

Since 2008, installation of utility-scale PV costs have fallen 64%, to a new low of $2.08/Watt. [4] These installed

costs have translated into record-low prices for electricity from solar power. Only ve years ago, contracts for

utility-scale PV power were commonly at ¢10/kWh. As of 2015 average prices are well below ¢5/kWh, with a

number of future projects already planned to deliver electricity below ¢3.5/kWh. It's important to note that these

low costs are reective in part of the location of projects in excellent solar resource locations and of the federal

investment tax credit (ITC).

Falling prices aren’t limited to the sunniest parts of the country either. While the majority of projects still arise from

the sunny Southwestern markets, 42% of new utility-scale PV power contracts signed since 2013 are east of the

Rocky Mountains, including Texas along with Southeastern and Midwestern parts of the country. [4]

Costs from reference [4]; Deployment from reference [16]. Costs shown are the median costs and exclude the eect of

the Investment Tax Credit. 1 gigawatt (GW) = 1,000 megawatts (MW). Costs and capacity are reported as DC power.

5 97.528 Quads of energy was consumed in the U.S. in 2015, [99] and the annual technical potential of utility-scale PV in the U.S. is estimated to be 282,800 TWh (equal to 965 Quads). [100]

6 Utility-scale PV capacity and cost gures are provided in terms of DC power unless otherwise indicated.

7 The average home consumed 10,932 kWh in 2014. [96]

Solar PV: Utility-Scale 5

In addition to expanding to new areas of the country, utility-scale PV is also being purchased by non-utility

consumers. Corporations are increasingly realizing the benets of directly procuring solar power from developers.

In 2015 more than 1,000 MW of solar PV capacity was contracted by corporations representing the retail, nance,

technology, and manufacturing industries, and this amount has quadrupled over the amount contracted in 2014.

[13] In 2016 it is predicted that over 1,000 MW of utility-scale PV will be contracted with non-utility customers,

[16] and it highlights how going solar increasingly makes business sense for many of these interested corporations.

Similarly, with support from the DOE’s Federal Energy Management Program, the Federal government is

increasingly directly contracting utility-scale PV. For example in 2015 the Department of the Navy procured

210 MW of a utility-scale PV project to support fourteen Navy installations in California. [19] Taken together,

these trends indicate how rapidly solar power is expanding: analysts expect that, for the rst time, over half of all

installations in 2016 will occur due to factors outside of Renewable Portfolio Standard obligations. [16]

Powerful Benefits

Utility-scale PV deployment to date have resulted in substantial environmental and human health benets. A recent

DOE study found that, in 2014, solar power saved 17 million metric tons of CO

2

, worth approximately $700

million in benets. In addition, there were another $890 million worth of benets from improved air quality due to

the reduction of air pollution thanks to the deployment of solar.

The study also found that water consumption was reduced by 7.6 billion gallons, equal to 0.5% of the total water

consumption from the power sector, with the majority occurring in drought stricken areas like California. When

looking at all of the benets together, they are worth over $1.5 billion dollars. [20]

In addition, the entire solar sector, inclusive of distributed and utility-scale PV, has provided immense economic

opportunities and has supported an estimated 220,000 domestic jobs at the end of 2015. [21] Similarly, the

manufacturing of solar photovoltaic modules and their components has added $1 billion in overall value to the

United States economy in just 2014. [8]

These benets continue to add up as deployment expands. For example, should the SunShot Vision scenario of

solar power providing 27% of all domestic generation by 2050 come to fruition, there would be an estimated $167

billion worth of savings through reduced health and environmental impacts. This includes preventing 25,000 to

59,000 premature deaths through 8-11% reduction in air pollution from power plants. [20] It could also bring

economic benets with total solar employment up to 335,000 jobs. [21]

A Bright Future

The amount of utility-scale solar projects in the pipeline is truly staggering. It took decades to achieve a cumulative

installation of 10,000 MW of PV, but it looks possible that 10,000 MW of utility scale solar will be installed this

year alone due to the previously anticipated expiration date of the investment tax credit. As of mid-2016, there

were more than 21,000 MW of utility-scale solar projects under development, with 8,400 MW of that total already

under construction. [22] With continued cost reductions and technology improvements, the future of this clean

energy technology is bright.

REVOLUTION...NOW

6 Solar PV: Distributed

Solar PV: Distributed

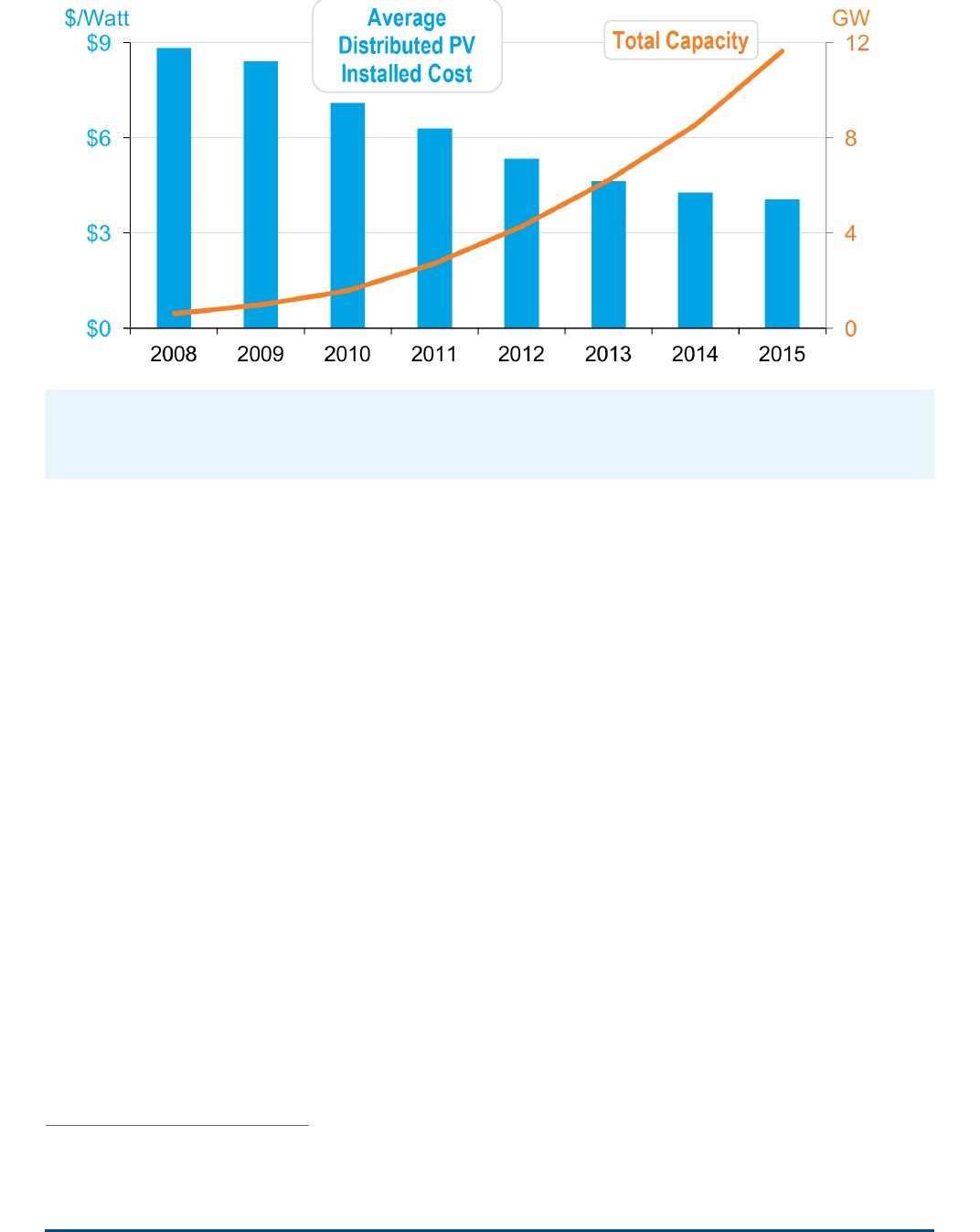

Shining On

Sunlight is available nearly everywhere and that means that unlike traditional power generating sources, solar

power can potentially be available anywhere there is sunshine. Distributed PV systems use the same basic PV

technology as larger utility-scale projects, but they can be small enough to t on a consumer’s rooftop. A robust

assessment of the available roof space in the US indicated that the total potential of electricity generation from

distributed rooftop PV is equal to 38.6% of the nation’s total electricity consumption. [24]

Although distributed PV technology has been available for years, falling prices over the last decade have unlocked

its potential not only for the average homeowner but for larger consumers like businesses and schools.

Many installations are small enough to t on a roof, but there is nothing tiny about distributed PV’s growth. Over

3,110 MW of distributed systems were installed in 2015, a 34% increase over 2014. [16] This past spring, the

millionth distributed PV system was installed, an indication of how widespread this technology has become. [25]

Through the end of 2015 a cumulative 11,638 MW had been installed in the United States, [18] generating an

estimated 12 billion kWh in 2015, and providing enough electricity to power over 1.1 million American homes.

Appraising Sunshine

The rise in installations of distributed solar has been enabled in part by a 54% reduction in installed cost since

2008. This reduction means the average installation was approximately $4.05/Watts in 2015 for residential systems.

[3] In addition it’s also important to note that this deployment trend is reective in part of the federal investment

tax credit (ITC) and supporting state policies such as net energy metering.

The cost reductions and supporting federal and state policies mean that more and more consumers are recognizing

the value of solar power. The value in terms of cost savings are well known: in 20 states and in 42 of America’s

50 largest cities, nancing a residential solar energy system currently costs less than purchasing electricity from a

Cost data from reference [3], deployment data from reference [16]. Costs are average installation costs for residential

sector PV and exclude the eect of the Investment Tax Credit. 1 GW = 1,000 MW.

8 Distributed PV capacity and cost gures are provided in terms of DC power unless otherwise indicated. In general distributed PV refers to capacity that is installed behind-the-meter and is less than 5 MWAC

in capacity, although individual references vary in their denitions.

9 The average home consumed 10,932 kWh in 2014. [95]

Solar PV: Distributed 7

customer’s local utility – commonly termed “grid parity”. [26, 27] However, the value of solar power is also being

recognized in new ways. Specically, research of real estate markets revealed that home buyers were willing to pay

$15,000 more for a home with an average-size solar photovoltaic system, equivalent to four additional dollars per

watt of solar power installed. [28, 29] The DOE’s Solar Training and Education for Professionals (STEP) program

is helping to ensure solar continues to be valued in the real estate market by educating agents and appraisers about

solar energy. [30] DOE has also funded tools to help the real estate professionals properly evaluate new and existing

distributed PV systems. [31]

Distributing Benefits

A number of actions have recently been undertaken to ensure that as the distributed solar market grows, all

consumers have access to clean energy opportunities. A recently announced Clean Energy Savings for All Initiative

aims to deploy 1,000 MW of solar to low- and moderate-income families by 2020. [32] In addition, almost 50%

of homes and businesses are not able to host their own solar system because they may be renters, might live in a

multi-family building with shared roof space, or simply don’t have an appropriate roof to host a PV system. [33]

For these consumers, community solar, also known as shared solar, allows groups of consumers to collectively own

shares of a single solar system located nearby. This enables them to share the benets of solar power. An analysis

shows that community solar could represent nearly half of the distributed solar market by 2020. [33] The recently

launched National Community Solar Partnership is working to bring together federal agencies, non-prots, and

private partners to unlock community solar’s potential in the nation. [34]

A Capital Idea

Another key factor in distributed PV comes not from technical innovations, but from advances in how consumers

can pay for solar power. Third-party-ownership of PV systems – where consumers lease a PV system instead of

purchasing it outright – has revolutionized the distributed PV market. This allows consumers to benet from lower

electricity payments without purchasing the whole PV system directly. The success of this model has been clear—

third-party nancing accounted for between 45%-90% of domestic residential PV systems installed in leading state

markets in 2015. [16] Continued development of new nancing options such as solar loans could lower the cost of

energy from distributed PV an additional 10%-20% over historical methods. [35] For example, Property Assessed

Clean Energy (PACE) programs allow homeowners to nance solar PV through no upfront cost and pay back the

loan through their property tax bills. Recent actions that provide guidelines for developing PACE programs, clarify

how Federal Housing Administration mortgage insurance and Veteran’s home loan guarantees apply to homes with

PACE assessments, and provide technical assistance to states and local communities will help further expand these

opportunities to make nancing solar easier for all Americans. [32]

Sunny Days Ahead

The deployment growth of distributed PV is expected to continue, as experts project the installed prices of

residential PV systems to fall an additional 16-33% by 2020. [36] Combined with innovative new nancing

and other solutions aimed at making distributed PV accessible to a wider array of consumers, this means more

Americans will have the opportunity to realize the wealth of benets provided by solar power.

REVOLUTION...NOW

8 LEDs

LEDs

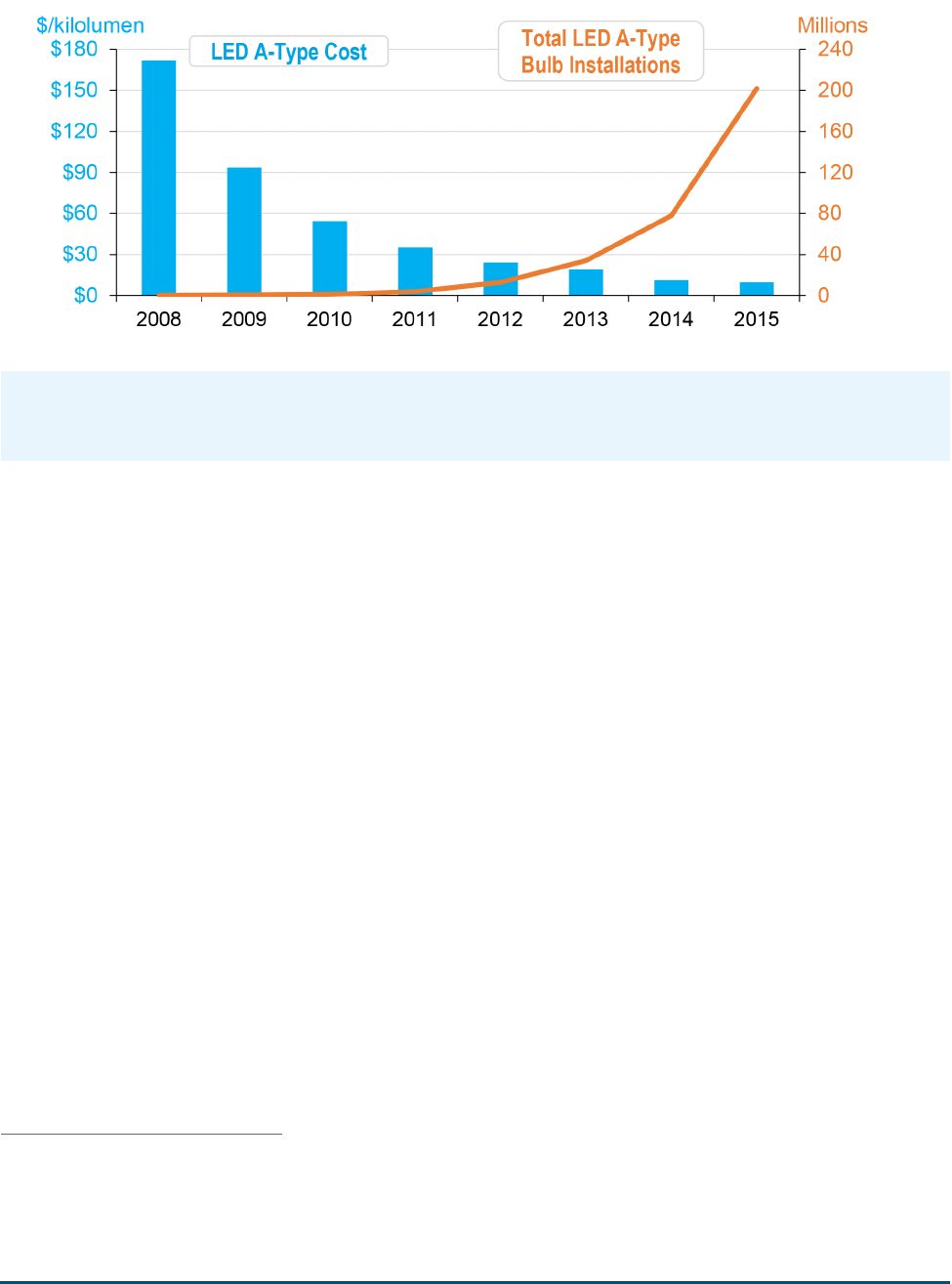

Turning Up the Lights

Stand underneath a traditional incandescent bulb and a LED bulb and you will soon feel the difference between

the two — heat. While both produce the same amount of light, the incandescent bulb is hot to the touch, a clear

sign that much of the energy it uses is being wasted. LED technologies have cut this wasted energy out of lighting:

the best performing 60 W equivalent LED bulbs available now consume 85% less energy than incandescent bulbs.

LEDs are spurring a dramatic change in lighting due to their vast energy savings potential, lower costs, improved

performance, and added benets like long lifetime and maintenance savings.

These benets are moving LEDs into the mainstream and drastically increasing their deployment. In one year, total

installations of common home LED bulbs more than doubled from 77 million to 202 million—a particularly rapid

growth considering there used to be fewer than 400,000 installations as recently as 2009. LED bulbs now account

for 6.0% of all currently installed A-type bulbs – growth enabled by an enormous 94% reduction in cost since 2008.

[5] Looking at the bigger picture across all LED product types, LED installations prevented 13.8 million metric

tons of CO

2

emissions and saved $2.8 billion in energy costs in 2015 alone.

This success is a direct result of research and development (R&D) investments made by both government and

industry that have brought down costs, improved efciency and performance, and fostered domestic manufacturing

of LED lighting components and products. Thanks in large part to these investments, the U.S. today is the hub of

LED lighting innovation. Today, America is beginning to reap the rewards of those years of investment.

Beyond the Bulb

While common A-type LED bulbs represent the largest number of LED installations, other lighting applications

have seen higher LED market penetration. For example, directional bulbs and large area outdoor lighting xtures

have LEDs penetrating 11% and 21% of installations respectively. However, a large number of installations does

Cost and deployment data from source [5]. “LED Bulb” refers to A-type bulbs. Kilolumen is a measure of visible light

output by a source. Price data is inflation adjusted to 2015 dollar-years.

10 In this report, “LED bulbs” refers to A-Type bulbs that are common in household applications.

11 Calculated from reference [101] See page 3, note 6. The best performing LED bulb approaches 90 lumens/W efcacy. To produce 800 lumens this LED draws 8.89 W of power, an 85% reduction compared to

the 60 W of power drawn by the equivalent incandescent bulb.

12 Emission savings calculated by converting the reported 278 trillion BTU of source energy savings from reference [5] to site energy using a 3.05 site-to-source ratio, converting to electricity savings using

3412 BTU/kWh, and multiplying by the national CO

2

emission intensity of 1,136 lbs CO2/MWh as reported by eGRID 2012. [102]

LEDs 9

not necessarily translate directly to the best opportunity for energy savings. Energy saving opportunities depends

not only on the number of installations, but also on the number of hours of operation and the energy efciency

improvement that LEDs offer over competing technologies. [37]

For all of these reasons, DOE and many in the lighting industry are looking toward potential energy savings in

the commercial and industrial sectors offered by replacing uorescent overhead lighting most commonly found in

ofces and manufacturing facilities. Energy impacts in these applications are disproportionately high in relation to

LED penetration because of the large number of installations and extended operating hours. In contrast to lighting

in homes, which average less than two hours of operation per day, commercial and industrial lighting xtures

average about 12 hours of operation per day. In 2015, LEDs in typical commercial and industrial lighting xtures

contributed 20% of the LED-enabled energy savings, despite representing only 3% of their respective market, and

are expected to contribute about 30% of the total energy savings from LEDs in 2035. [37]

Achieving the greatest possible market adoption and energy savings from LED products will require ongoing

technology R&D improvements. Unlike conventional lighting sources, LED technology has signicant headroom

for additional technological advancements. DOE is committed to working with industry to continue to reduce

costs through improved materials and optics, optimized product design and assembly, boosting lumen outputs, and

integrating LEDs with lighting control systems, which will enable even greater energy savings. DOE analysis has

shown that with aggressive research and development, LED product efciency can still be more than doubled, from

the current 95 lumens per watt to 218 lumens per watt. [5]

A Bright Idea

Fully capitalizing on the promise of LED technology will catapult our nation toward creating a clean energy

future. Energy-efcient technologies like LED lighting not only reduce the consumption of fossil fuels, they also

go hand-in-hand with effectively using renewable energy. For example, further cost reductions in LED lighting

will make it far more affordable and practical to construct zero-energy buildings. These buildings are so energy

efcient that renewable energy systems can help to offset all or most of their annual energy consumption. Likewise,

the conversion to LED street lighting will enable cities and towns across the country to dramatically reduce their

energy and maintenance costs. Developing this technology domestically also allows American manufacturers to

benet from exporting LEDs to rapidly developing nations while enabling those countries to save money and cut

emissions by leapfrogging over less efcient lighting technologies.

LEDs are projected to make up over 85% of the nation's lighting installations by 2035, driven by performance

increases and cost savings relative to conventional lighting. If DOE's Solid State Lighting Program targets for

LEDs are met, the market penetration of LEDs is projected to drive a 75% reduction in annual lighting energy

consumption by 2035 over a scenario without LEDs. This would result in total annual energy savings nearly

equivalent to the energy consumed by 45 million American homes. The cumulative savings from 2015 through

2035 would save Americans nearly $630 billion in avoided energy costs, illuminating the potential of LEDs to save

energy, save money, and enable a clean energy future. [37]

REVOLUTION...NOW

10 Electric Vehicles

Electric Vehicles

Electrifying Success

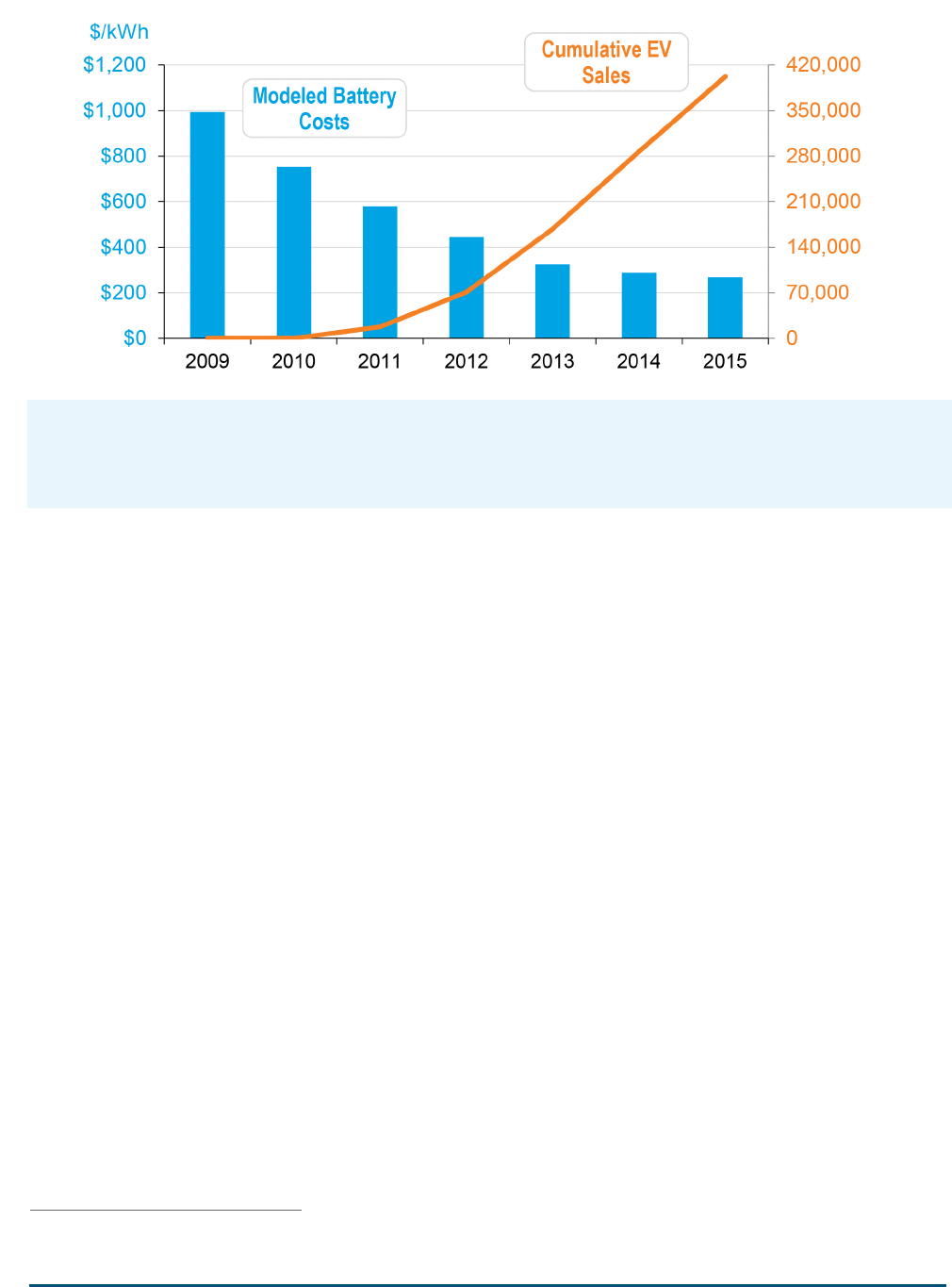

Americans bought over 115,000 electric vehicles (EVs) in 2015, more than double the number purchased in 2012

despite sustained low gasoline prices. This brought the total number of EVs on the U.S. roads to over 400,000

by the end of 2015. Sales were represented by over 20 EV model types available from over 15 different brands.

[38] EV deployments continue to expand with cumulative sales topping 490,000 as of August 2016. [7] Today,

EVs are helping to support America’s energy and climate goals and are providing an opportunity for domestic

manufacturers to remain globally competitive in the 21st century.

This is good news for our climate, our health, and our economy. With fewer to no tailpipe emissions, EVs reduce

local air pollution and help us breathe a little easier. They also enhance our energy security by reducing our oil use,

while substantially cutting carbon emissions. For example, an EV on average reduces greenhouse gas emissions

by 58%, compared to a gasoline fueled car. EVs also will become cleaner as the nation’s electricity supply is

projected to continue to move to lower-emitting energy sources. [23] The development and production of EVs is

also contributing to the economy – the United States is the largest market for automotive lithium-ion batteries and

lithium ion battery manufacturing has added about $400 million in value to the nation's economy in 2014. [8]

This continued growth is the direct result of combined federal, state, and industry efforts to bring down the

cost of EVs through research and better battery development, drivetrain improvements, promoting consumer

adoption through tax credits and other incentives, and supporting public and private investments in domestic EV

manufacturing capacity. DOE’s utility partnership agreements with Edison Electric Institute and the American

Public Power Association are intended to pick up this pace. DOE is also developing plans to collaborate with

utilities to accelerate EV and charging infrastructure deployment. [39] The continued collaboration and investment

in public education and outreach initiatives along with industry, state and federal support build on these successes

to ensure the continued increase in EV adoption.

Costs are modeled costs for high-volume battery systems, derived from DOE/UIS Advanced Battery Consortium PHEV

Battery development projects and are representative of nominal dollars. Sales as reported in reference [38]. “EVs” include

all plug-in hybrid and battery plug-in vehicles.

13 EV emissions are highly sensitive to geographic location; this number is based on the emissions associated with the national electricity generation fuel mix as reported in reference [103].

Electric Vehicles 11

Charging Ahead

The increase in EV sales in recent years has been enabled by the development of lower-cost lithium-ion batteries.

DOE estimates the cost of EV batteries produced at high volume has fallen by an astounding 73% since 2009.

The cost and performance of batteries are key factors in continuing to lower the costs of EV ownership. In addition

to universities and industry, DOE has been a leader in battery R&D investment: between 1992 and 2012, DOE

invested $1 billion in battery R&D, which advanced the state-of-the-art by six years and created $3.5 billion worth

of economic value. This investment continues to pay off as battery costs may be as low as $200/kWh by 2020.

[40] Looking ahead, DOE will work with industry, academia, and its national laboratories toward achieving an

even more aggressive goal of $125/kWh modeled production costs by 2022. [41]

We can already see rsthand the results of advanced research in EV batteries as it makes its way into the market.

For example, improvements in battery energy density enabled by DOE funded research has allowed the energy

storage capacity of the second-generation Chevrolet Volt battery to be increased by 15% compared to the previous

generation. [42] In general, optimization of cell chemistry, design, and performance decreases the mass of battery

packs, allowing EVs to travel farther with full performance. Automakers are taking advantage of these innovations

to design lower-priced EVs that are poised to be strong competitors. For example, multiple automakers plan

on delivering 200-mile-range EVs for less than $40,000 around 2017. [43] As EVs accounted for 1.5% of all

passenger cars sold in 2015, the potential for the next generation of EVs to impact transportation is signicant.

Power Up

Improved and expanded charging infrastructure will also maintain the momentum for EVs. There are now more

than 35,000 public and private EV charging outlets in the United States. Of those, there were over 4,000 DC fast

chargers, which allow drivers to charge up to 100 miles of range in as little as 20 minutes.[44, 45]

In 2015, the DOE Workplace Charging Challenge had 605 workplaces from partner organizations that have

committed to providing EV charging for employees, increasing range condence for potential EV owners. [46]

This effort has shown increased deployment as employees of challenge partners were six times more likely to

drive an EV than the average worker. [46] EV owners with access to workplace charging also drive 23-26% more

electric-powered miles than those that do not. [47] Moving forward workplace charging while increasing EV

infrastructure is key to enabling future EV deployment and emissions reductions. Recent analyses of workplace

charging show that in some areas, charging during the workday reduces EV emissions. [48]

Road to the Future

Driven by reduced battery and vehicle costs, as well as an expanded charging network, EVs are continuing to

attract new consumers and provide environmental and economic benets.

Looking ahead, continued cost reductions and performance improvements of EVs coupled with new technologies,

such as wireless charging, will increase the performance and attractiveness of EVs. With over 490,000 EVs

deployed as of August 2016, [7] the half-million EV milestone will certainly be passed before the end of the

year. America is one of the largest EV markets in the world, and more Americans are powering their cars with

affordable, clean, and secure energy.

14 Estimated costs are modeled and validated through applied research, and represent calculated high-volume commercial production costs, rather than market price.

15 Ination adjusted to 2015 dollars using U.S. Bureau of Economic Analysis GDP budget deator. Data from reference [104].

16 115,262 EVs sold in 2015 as reported in reference [38] as compared to 7,525,023 passenger cars sold in 2015 as reported by Ward’s Auto in reference [105].

REVOLUTION...NOW

12 Revolution Next

Revolution Next

The technologies highlighted in the rst section of this report have already made a big impact and are easily visible

in our daily lives. Wind towers dot the landscape, solar panels sprout on rooftops, LEDs are on shelves in every

hardware store, and the latest EV models drive through neighborhood streets.

Other emerging technologies have not quite reached the same wide-scale deployment, or are impacting our energy

use in ways that are not as visible in our daily lives. Yet in each case, deployment has begun to accelerate, costs

have started falling, and large-scale deployment could transform portions of the energy sector.

Last year, this report highlighted fuel-efcient technologies for heavy trucks, smart building controls, and vehicle

lightweighting. Along with updates in these areas, this report will look to highlight the accomplishments and

potential of fuel cells, industrial energy management, grid-scale batteries, and big area additive manufacturing.

The technologies we discuss from this point forward are what we believe we should keep an eye on over the next

ve to 10 years.

Super Trucks

The SuperTruck Initiative — a DOE program to increase long-haul 18 wheeler truck fuel efciency by 50%

over 2009 levels — has been incredibly successful. All of the teams will exceed this goal by the end of 2016,

with one team achieving a 115% increase in fuel efciency. The success of the initiative has already encouraged

participating companies to commercialize technologies from SuperTruck. For example, Volvo has commercialized

tractor aerodynamic improvements in its 2016 highway trucks [49] and several engine improvements will be

commercialized for 2017. [50, 51] Peterbilt used its aerodynamics work in SuperTruck to develop a high-efciency

truck package for its Model 579 tractor. [52] Their work was commercialized in 2014 and has been continually

rened since then. It includes extensive aerodynamic features such as tractor side fairings that close gaps between

the fender and front steer wheels, a front air dam to prevent air from owing under the truck, and fairings that

extend down the side of the tractor nearly to the ground, to direct airow away from the underside of the truck.

Overall the participating teams have already successfully commercialized 21 technologies to date, including

advances in engine and drivetrain integration and in aerodynamics. An additional 26 technologies are estimated

to be commercialized in the next two to four years, and 13 more in the ve to 10 year timeframe, highlighting the

potential of these technologies to impact fuel use in heavy-duty vehicles. [53]

Building on the success of the SuperTruck I initiative, in August of 2016, DOE announced a follow-on SuperTruck

II $80 million program for research, development and demonstration of long-haul tractor-trailer truck technology.

These projects will research, develop, and demonstrate technologies to improve heavy-truck freight efciency by

more than 100 percent, relative to a manufacturer’s best-in-class 2009 truck, with an emphasis on technology cost-

effectiveness and performance. DOE has made four selections under this opportunity Cummins, Inc. with Peterbilt

Trucks as a partner; Daimler Trucks North America LLC; Navistar, Inc.; and Volvo Technology of America LLC.

[54] Another $12 million supported projects on the research, development, and demonstration of plug-in electric

powertrain technologies for medium- and heavy-duty vehicles. [55]

Smart Buildings

Buildings are full of hidden energy savings potential that are easy to overlook because they are housed in familiar

technologies, such as heating, ventilation, and air conditioning equipment. However, with sophisticated software

and advanced data and analysis being applied to everyday building operations, building owners can leverage the

more than 58.5 million smart meters installed in the nation to realize the cost-saving benets of analytics. [56]

Recently, the Energy Department launched the Smart Energy Analytics Campaign to provide technical support

and recognition for owners in their use of a wide variety of commercially available Energy Management and

Information Systems (EMIS) technologies. [57] Paired with ongoing monitoring practices, these technologies help

identify energy-saving opportunities and improve building performance for the long run. The potential for EMIS

to save energy is also sizable: as much as 10-20% energy savings is possible in a single building, and if EMIS best

Revolution Next 13

practices were adopted by all target buildings in the U.S. commercial sector, over $4 billion in cost savings could

be achieved. [58] From single buildings to large portfolios, owners are moving building energy and operations into

the age of smart, ongoing, data-centered analytics.

Lightweighting Materials

The development and use of lightweighting materials, such as high strength steel, aluminum, and carbon ber, has

the potential to reduce total mass of a vehicle, increase its fuel efciency, while maintaining or evening improving

vehicle safety. [59] For example, a 10% reduction in vehicle weight can result in a 6-8% improvement in fuel

economy, and can also allow electric powered vehicles to go further on a single charge. [60] Using lightweight

components is also benecial because it means vehicles can carry additional advanced emission control systems,

safety devices, and integrated electronic systems to increase functionality, safety, and performance without

increasing the overall weight of the vehicle.

Overall the use of lightweight materials in vehicles is on the rise. The average amount of regular steel in a vehicle

was reduced by over 200 lbs since 1995, while average amount of high and medium strength steel used per vehicle

increased by 325 lbs. Similarly the amount of plastics and composites used per vehicle increased by 40% since

1995. This trend continues — in addition to the 2016 Ford F-150 that used aluminum to shed nearly 700 lbs, the

2017 Chrysler Pacica minivan was reengineered with a new body and vehicle platform to reduce weight and

improve vehicle fuel economy. The Pacica is 250 lbs lighter than the Town & Country – the previous minivan

offering from Chrysler. Part of this weight reduction comes from use of lightweight magnesium in place of steel in

the rear liftgate. This reduced the liftgate weight by 22 lbs all while maintaining crash safety performance. [61]

Through industry, academia, and national laboratories, the Department of Energy continues to invest in

technologies to spur the development and commercialization of lightweight materials. The recently completed

Multi-Material Lightweight Vehicle (MMLV) project demonstrated the ability to combine several advanced

lightweight materials, resulting in a vehicle that is 23.5% lighter than a similar mid-sized sedan. This prototype

vehicle passed several major safety tests and has already led to several of these technologies being used in vehicles

on the market. [62] Built by Vehma International and Ford, with support from DOE’s Vehicle Technologies Ofce,

the MMLV demonstrated the feasibility of integrating lightweight materials and joining technologies into current

production vehicles. The MMLV and the technologies used in it offer the potential to make our vehicles lighter and

more efcient for generations to come.

REVOLUTION...NOW

14 Revolution Next

Stacked for Success: Fuel Cells

Fuel cells convert the chemical energy from fuel directly into electricity, without the need for combustion, thereby

generating power at high efciencies and with low or even zero emissions. They can use diverse domestic resources

for fuel and because they’re scalable, they can be small enough to power a vehicle and large enough to support

power plants.

For the rst time in history, automakers have introduced commercial fuel cell electric vehicles (FCEVs) that

regular consumers can purchase or lease. These cars run on hydrogen, produce zero pollution from the tailpipe,

can be fueled in just a few minutes, and can travel more than 300 miles on a single ll. Toyota is currently selling

the Mirai and Hyundai is leasing its SUV, the Tucson, in California. [38] In addition, the Honda Clarity will be

available in late 2016, while Daimler, General Motors, BMW, and others plan to bring FCEVs to market soon.

[65-68] There are also several hydrogen-fueled medium and heavy vehicles - including transit buses - available on

the market today. [38] These FCEVs can already cut total greenhouse gas emissions by 50% compared to today’s

conventional cars, even if hydrogen is produced from natural gas. When hydrogen is produced from renewables or

low carbon sources, greenhouse gas emissions can be reduced more than 90%. [69]

DOE has funded research enabling signicant improvements in the technology: platinum is the most expensive

material used in fuel cells, and the amount needed was cut by ve-fold enabling a 50% reduction in costs since

2007 while quadrupling durability. [70] DOE has validated more than 200 FCEVs driving over 6 million miles,

demonstrating cutting edge advances under real world conditions. In addition, Recovery Act funds helped cost

share 1,600 fuel cells that enabled 18,000 more used in forklifts and backup power units. [72, 73] In 2015,

commercial fuel cell shipments surpassed 60,000 units worldwide, demonstrating growing traction in the

marketplace. [64]

As fuel cells gain traction, more work is underway to further reduce platinum metals, cut costs, and improve

durability. While today millions of tons of hydrogen is produced from cheap natural gas, R&D is focused on

low-cost hydrogen produced from fully carbon-free pathways. Continued innovation in production, delivery, and

storage will drive wider deployment of clean fuel cell technologies.

Cost data is modeled fuel cell cost at high volume in nominal dollars from reference [63] . Deployment data is global fuel

cell shipments for stationary, portable, and transportation uses from reference [64].

Revolution Next 15

ISO 50001 and the Superior Energy Performance Program in the

Manufacturing Sector

The industrial sector currently consumes 32% of all energy consumed in the country. [18] Capital funded energy

efciency projects do result in savings but experience has shown that the energy performance gains from these

various one-off energy efciency projects do not deliver sustained energy performance improvements due to a

lack of continual post implementation monitoring and optimization. [75, 76] In order to ensure sustained energy

performance gains, energy should not be considered a xed operational expense but managed just as carefully done

for production, quality, and safety. [78]

The International Organization of Standardization (ISO) has developed ISO 50001, a data driven management

system standard that provides a exible framework for organizations to implement an energy management

system (EnMS) that can integrate with existing business practices. An EnMS achieves energy savings through a

systematic evaluation of signicant energy uses, review of operations, and maintenance and performance of each

system. Conformance with ISO 50001 requires continual improvement to both the management system and energy

performance improvement. DOE’s Superior Energy Performance (SEP) program provides additional guidance,

tools, and protocols to drive deeper, more sustained savings from ISO 50001.

ISO 50001 and the SEP program achieve signicant energy and CO

2

emission savings results – all through better

management of energy across facilities and organizations. In many cases, the improvements are achieved with no

or low cost actions which existing facility staff can implement. Today, SEP certied facilities have achieved a 12%

reduction in energy expenditures within 15 months of implementation of ISO 50001, equating to an annual savings

of $36,000 to $938,000 using no-cost or low-cost operational measures. [78] More broadly, facilities with annual

energy costs greater than $2 million can expect investment payback on ISO 50001 in less than 1.5 years. [79]

The potential for energy management through ISO 50001 to impact energy use and emissions is enormous – broad

global deployment could save over $600 billion in energy costs, and 6,500 million tons of CO

2

by 2030. This

is equivalent to removing the annual emissions of 215 million passenger vehicles. [80] A new global campaign

announced at the 2015 Clean Energy Ministerial aims for 50,001 certications by 2020, [81] highlighting the

universal opportunity for economies around the world to realize energy savings, cost savings, and move the world

towards a clean energy future.

Data for global ISO 50001 certifications from reference [74]; SEP certifications provided by SEP program manager.

REVOLUTION...NOW

16 Revolution Next

Supercharging the Grid with Batteries

As variable renewable generation from wind and solar continues to increase, the electricity grid needs more

exibility – making it better able to support variable generation and to respond to the complex needs of our

electricity system. Specialized batteries are one technology that can provide this type of exibility which can

signicantly improve the operating capabilities to the grid. Their ability to store electricity produced at one time

for use at another time is key, allowing them to support deployment of renewable generation like wind and solar,

as well as improving the overall efciency and quality of the power grid. Batteries can also be sized and located in

local communities or at a customer’s location making them invaluable for emergency preparedness and resiliency

in case of grid disruptions due to severe weather or other events. [83, 84]

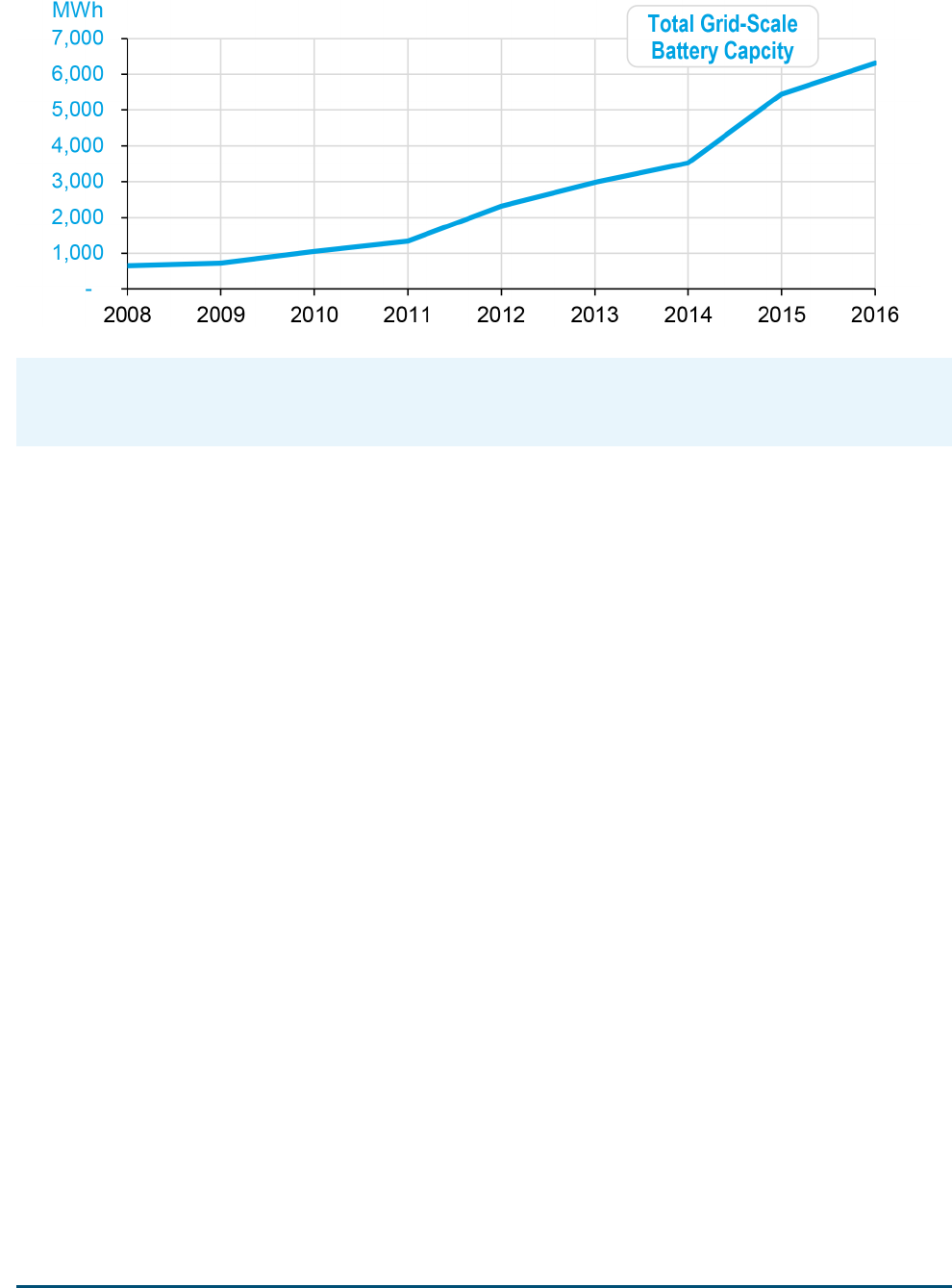

The capacity of these grid-scale batteries has increased nearly 10-fold since 2008, [83] and they are already

enhancing the capabilities of the grid. The lithium-ion battery packs used in the majority of grid-connected batteries

have declined in cost by about 60% between 2007 and 2014 [40] and analysts expect both utility and consumer

scale batteries to decline in cost by another 20-27% in just the next two years. [85] With these cost reductions and

further deployment the total domestic energy storage market could be worth $2.9 billion by 2021, as compared to

$350 million in 2015. [85]

DOE continues to support innovative energy storage solutions in a number of avenues, such as R&D in the Ofce

of Electricity Delivery and Energy Reliability’s Energy Storage program [86] and through the Advanced Research

Projects Agency - Energy (ARPA-E) Grid-scale Rampable Intermittent Distpatchable Storage (GRIDS) program

area. [87] More recently DOE’s SunShot program awarded $18 million in 2016 to develop energy storage solutions

for solar power using battery and other technologies, with the goal of developing projects to enable essentially “on-

demand” solar power. [88] Continued innovation and deployment of grid scale batteries on the grid will provide

added exibility to help support the evolving of a clean energy electricity system.

Battery capacity data from DOE Energy Storage Database, [82] showing only domestic electrochemical projects listed as

“operational” by year project was commissioned.

Revolution Next 17

Big Area Additive Manufacturing

Manufacturing is a key sector of the economy that will both enable a clean energy future and present opportunities

for further energy savings. The manufacture of specic complex parts has traditionally relied on “subtractive”

processes—taking solid blocks of metal and cutting away the unnecessary parts to sculpt the nal products.

Additive manufacturing (AM)—also known as 3-D printing—turns this process on its head by building items using

advanced techniques that add raw material only where needed. While AM provides energy savings through reduced

amounts of material needed and reducing the number of production steps, it has the potential to unlock signicant

energy savings through unprecedented design exibility that is unavailable to conventional manufacturing

techniques. [89, 90]

New advances in technology are literally expanding the potential of AM by increasing the size of components

that can be manufactured. Big Area Additive Manufacturing (BAAM) – developed in partnership with Cincinnati

Incorporated, the Department of Energy, and Oak Ridge National Lab – can construct items up to 10 times larger.

[91] These items can also be produced at nearly 99% less energy per unit of mass as compared to other commonly

used but smaller industrial AM techniques and even uses less energy than common conventional manufacturing

processes like polymer injection molding. The lower energy intensity of BAAM arises because BAAM does not

heat an oven during manufacturing, and generally operates at lower temperatures and pressures.

In addition to being less energy intensive and faster than conventional methods, BAAM is enabling the next-

generation of design and manufacturing for other clean energy technologies. For example, creating molds for

advanced wind turbine blades are complex, energy-intensive, and time-consuming. BAAM can produce these

molds 500 to 1000 times faster than other industrial additive techniques, and overall can simplify the manufacturing

of molds for turbine blades. This would reduce the costs and amount of time required for blade manufacture, as

well enabling further and more rapid innovation in blade design. [91, 92] BAAM was also a key element in the

Additive Manufacturing Integrated Energy demonstration projection, showcasing how rapid design and prototyping

can enable new innovations in the buildings, transportation, and renewable sectors. [93]

The aerospace sector also holds a large potential for BAAM to revolutionize manufacturing while saving energy.

BAAM was recently used by Oak Ridge National Laboratory to produce a tool used by Boeing for use in the

manufacture of airplane wings, which secured a spot in the Guinness Book of World Records as the world’s largest

3D-printed object. [94] The tool was produced in signicantly less time and at lower cost than by conventional

techniques, and will be used by Boeing in the production of their new 777X aircraft. This exemplies how the

widespread adoption of BAAM and other AM techniques in the aerospace sector could result in 92.1–215.0 million

metric tons of avoided CO

2

emissions. [95]

Though the aerospace sector could be a likely rst adopter for AM technologies, the broader manufacturing sector

will also benet as cost and performance improve. Any product with complex, highly customized, lightweight,

or hard to manufacture components may stand to benet from AM, especially when considering the reduced time

to market, quick prototyping, waste minimization, on-site production, and on-demand manufacturing benets that

come along with the techniques. [90] DOE is particularly focused on applications in clean energy manufacturing

such as metal and composite tooling and molding, lightweight automotive components, renewable and efcient

energy generation systems, materials for extreme environments in industrial processes, and in buildings

technologies. BAAM exemplies the potential future of advanced manufacturing, allowing us to innovate and

manufacture things bigger, stronger, faster, and with less waste, to enable a clean energy future.

REVOLUTION...NOW

18 Conclusion

Conclusion

The clean energy technologies highlighted here are transforming how our nation produces and uses energy. While

challenges exist for these technologies, it is clear they are not long-term opportunities, but a signicant part of the

energy landscape right now. We can and should plan on using them to clean our air, drive energy independence, and

help build an economy that is more competitive and more efcient, all while reducing carbon pollution.

There are even more technologies that are just on the horizon that will be every bit as important to the future

clean energy economy. DOE will continue to encourage these innovations by providing support for R&D, policy

development consumer education, and industry and stakeholder engagement. With continued progress in critical

renewable and energy-efcient technologies like these, we can look forward to a future of clean, American-made

energy.

References 19

References

[1] M. Bolinger and R. Wiser, Memorandum - Documentation of a Historical LCOE Curve for Wind in Good

to Excellent Wind Resource Sites, Lawrence Berkeley National Laboratory, 2012 - Updated Feb. 10, 2014.

[2] C. Moné and E. Lantz, Draft - Fiscal Year 2016 WWPTO LCOE Reporting Memorandum, National

Renewable Energy Laboratory, 2016.

[3] G. L. Barbose and N. R. Darghouth, Tracking the Sun IX: The Installed Price of Residential and Non-

Residential Photovoltaic Systems in the United States, Lawrence Berkely National Laboratory, August

2016. http://go.usa.gov/xKDP9.

[4] M. Bolinger and J. Seel, Utility-Scale Solar 2015: An Empirical Analysis of Project Cost, Performance,

and Pricing Trends in the United States, Lawrence Berkeley National Laboratory, August 2016. http://

go.usa.gov/xKncY.

[5] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Solid-State Lighting

R&D Plan, June 2016. http://go.usa.gov/xZeQz.

[6] U.S. Department of Energy, Energy Information Administration, "Wind adds the most electric generation

capacity in 2015, followed by natural gas and solar," Today In Energy, March 23, 2016. http://go.usa.gov/

xKeRu.

[7] Y. Zhou, Light Duty Electric Drive Vehicles Monthly Sales Updates, Argonne National Laboratory,

Accessed September 2016. http://go.usa.gov/c3PeV.

[8] Clean Energy Manufacturing Analysis Center. Benchmarks of Global Clean Energy Manufacturing,

National Renewable Energy Laobratory. Forthcoming.

[9] R. Wiser and M. Bolinger, 2015 Wind Technologies Market Report, Lawrence Berkeley National

Laboratory, 2016. http://go.usa.gov/xZPwB.

[10] American Wind Energy Association, U.S. Wind Industry Annual Market Report Year Ending 2015, April

2016. http://www.awea.org/amr2015.

[11] U.S. Department of Energy, Enabling Wind Power Nationwide, May 2015. http://go.usa.gov/3SRMj.

[12] U.S. Department of Energy & U.S. Department of the Interior, National Offshore Wind Strategy,

September 2016. http://go.usa.gov/xZPKV.

[13] The Business Council for Sustainable Energy, Sustainable Energy in America Factbook, 2016, http://www.

bcse.org/sustainableenergyfactbook.

[14] U.S. Department of Energy, Wind Vision, May 2015. http://energy.gov/eere/wind/wind-vision.

[15] R. Wiser, K. Jenni, J. Seel, E. Baker, M. Hand, E. Lantz and A. Smith, “Expert elicitation survey on

future wind energy costs," Nature Energy, vol. 1, p. 16135, 2016. http://www.nature.com/articles/

nenergy2016135.

[16] GTM Research and Solar Energy Industries Association, U.S. Solar Market Insight: 2015 Year-in Review,

March 2016. http://www.seia.org/research-resources/solar-market-insight-2015-q4.

REVOLUTION...NOW

20 References

[17] U.S. Department of Energy, Energy Information Administration, Monthly Energy Review, “Table 1.1.A:

Net Generation from Renewable Sources,”August 2016. http://go.usa.gov/cYAZm.

[18] Federal Energy Regulatory Commission, Ofce of Energy Projects, Energy Infrastructure Update for June

2016, July 2016. http://go.usa.gov/xKnYY.

[19] U.S. Navy; Energy, Environment and Climate Change. Offsite California Renewable Energy Purchase.

Accessed September 2016. http://go.usa.gov/xKtqB.

[20] R. Wiser, T. Mai, D. Millstein, J. Macknick, A. Carpenter, S. Cohen, W. Cole, B. Frew and G. A. Heath,

On the Path to SunShot: The Environmental and Public Health Benets of Achieving High Penetrations of

Solar Energy in the United States, National Renewable Energy Laboratory, May 2016. http://go.usa.gov/

xKDQk.

[21] D. Chung, K. Horowitz and P. Kurup, On the Path to SunShot: Emerging Opportunities and Challenges in

U.S. Solar, National Renewable Energy Laboratory, May 2016. http://go.usa.gov/xKDUC.

[22] GTM Research and Solar Energy Industries Association, Solar Market Insight Report 2016 Q2, June 2016.

http://www.seia.org/research-resources/solar-market-insight-report-2016-q2.

[23] U.S. Department of Energy, Energy Information Administration, Annual Energy Outlook 2016, September

2016. http://go.usa.gov/xKDUF.

[24] P. Gagnon, R. Margolis, J. Melius, C. Phillips and R. Elmore, Rooftop Solar Photovoltaic Technical

Potential in the United States: A Detailed Assessment, National Renewable Energy Laboratory, January

2016. http://go.usa.gov/xKngV.

[25] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, With 1 Million Solar

Projects Across America, SunShot Shines On, May 2016. http://go.usa.gov/xKDEB.

[26] J. Kennerly and A. Proudlove, Going Solar in America: Ranking Solar's Value to Consumer's in America's

Largest Cities, NC Clean Energy Technology Center, January 2015. https://nccleantech.ncsu.edu/wp-

content/uploads/Going-Solar-in-America-Ranking-Solars-Value-to-Customers_FINAL1.pdf.

[27] C. Honeyman, U.S. Residential Solar Economic Outlook 2016-2020: Grid Parity, Rate Design

and Net Metering Risk, GTM Research, February 2016. http://www.greentechmedia.com/research/report/

us-residential-solar-economic-outlook-2016-2020.

[28] S. Adomatis and B. Hoen, Appraising into the Sun: Six-State Solar Home Paired-Sales Analysis, Lawrence

Berkeley National Laboratory, November 2015. http://go.usa.gov/xKDVF.

[29] B. Hoen, G. T. Klise, J. Graff-Zivin, M. Thayer, J. Seel and R. Wiser, Exploring California PV Home

Premiums, Lawrence Berkeley National Laboratory, December 2013. http://go.usa.gov/xKDp3.

[30] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, SunShot Programs Bring

Solar Energy Basics to Real Estate Pros, July 2016. http://go.usa.gov/xKDpT.

[31] Sandia National Laboratories, PV Value Tool, Accessed August 2016. http://go.usa.gov/xZs2w.

[32] The White House, Ofce of the Press Secretary, Fact Sheet: Obama Administration Announces Clean

Energy Savings for All Americans Initiative, July 2016. http://go.usa.gov/xKDpA.

References 21

[33] D. Feldman, A. M. Brockway, E. Ulrich and R. Margolis, Shared Solar: Current Landscape, Market

Potential, and the Impact of Federal Securities Regulation, National Renewable Energy Laboratory, April

2015. http://go.usa.gov/xKDvh.

[34] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, National Community

Solar Partnership, Accessed September 2016. http://go.usa.gov/xKDwk.

[35] D. Feldman and M. Bolinger, On the Path to SunShot: Emerging Opportunities and Challenges in

Financing Solar, National Renewable Energy Laboratory, May 2016. http://go.usa.gov/xZFHQ.

[36] D. Feldman, G. Barbose, R. Margolis, M. Bolinger, D. Chung, R. Fu, J. Seel, C. Davidson, N. Darghouth

and R. Wiser, Photovoltaic System Pricing Trends: Historical, Recent, and Near-Term Projections,

National Renewable Energy Laboratory, August 2015. http://go.usa.gov/xZMRx.

[37] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Energy Savings Forecast

of Solid-State Lighting in General Illumination Applications, Prepared by Navigant Consulting, September

2016. http://go.usa.gov/xZeez .

[38] Oak Ridge National Laboratory, 2015 Vehicle Technologies Market Report, April 2016.

http://go.usa.gov/xZhDF.

[39] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Energy Department and

Edison Electric Institute Sign Agreement to Advance Electric Vehicle Technologies, June 2015.

http://go.usa.gov/xZhBx; Energy Department and American Public Power Association Sign Agreement to

Accelerate Growth of Electric Vehicle Market. July 2016. http://go.usa.gov/xKtqv.

[40] B. Nykvist and M. Nilsson, "Rapidly falling costs of battery packs for electric vehicles," Nature Climate

Change, vol. 5, pp. 329-332, 2015. http://dx.doi.org/10.1038/nclimate2564.

[41] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, EV Everywhere Grand

Challenge, January 2014. http://go.usa.gov/3Sn3B.

[42] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, EERE Success Story—

Battery Cathode Developed by Argonne Powers Plug-in Electric Vehicles, August 2015. http://go.usa.gov/

xKtqS;General Motors, Chevrolet Introduces All-New 2016 Volt, January 12, 2015. Accessed August 25,

2015. http://media.gm.com/media/us/en/gm/news.detail.html/content/Pages/news/us/en/2015/Jan/naias/

chevrolet/volt/0112-volt-2016-intro.html.

[43] A. Davies, Chevy Could Beat Tesla to Building the First Mainstream Electric Car, Wired, January 13,

2015. Accessed August 21, 2015. http://www.wired.com/2015/01/chevrolet-bolt-ev.

[44] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Alternative Fueling

Station Counts by State, Alternative Fuels Data Center, Accessed August 2016. http://go.usa.gov/3S7rh.

[45] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, EV Everywhere: Vehicle

Charging, Accessed September 2015. http://go.usa.gov/xB35w.

[46] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Workplace Charging

Challenge Mid-Program Review, December 2015. http://go.usa.gov/xB3NH.

REVOLUTION...NOW

22 References

[47] Idaho National Laboratory, Plugged In: How Americans Charge Their Electric Vehicles, September 2015.

http://go.usa.gov/xB3cm.

[48] J. McLaren, J. Miller, E. O’Shaughnessy, E. Wood and E. Shapiro, Emissions Associated with Electric

Vehicle Charging: Impact of Electric Generation Mix, Charging Infrastructure Availablility, and Vehicle

Type, National Renewable Energy Laboratory, April 2016. http://go.usa.gov/xB3VY.

[49] P. Amar, Volvo - Supertruck, Volvo Group North America, June 16, 2016. http://go.usa.gov/xKQcT.

[50] J. Gibble and P. Amar, SuperTruck Powertrain Technologies for Efciency Improvement, 2016 Annual

Merit Review, June 2016. http://go.usa.gov/xKQc9.

[51] Volvo Trucks, Volvo Uses Knowledge Gained from SuperTruck to Increase Efciency, Performance in

2017 Powertrain Lineup, April 2016. http://www.volvotrucks.us/about-volvo/news-and-events/

knowledge-gained-from-supertruck-to-increase-efciency-performance-in-2017-powertrain-lineup/.

[52] S. Kilcarr, Aerodynamism and Peterbilt's Model 579 EPIQ tractor, FleetOwner, August 2015.

http://eetowner.com/equipment/aerodynamism-and-peterbilts-model-579-epiq-tractor#slide-0-

eld_images-169321.

[53] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, SuperTruck Success -

Progress on Fuel Efciency and Market Adoption, June 2016. http://go.usa.gov/xBCEF.

[54] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Energy Department

Announces $137 Million Investment in Commercial and Passenger Vehicle Efciency, August 2016.

http://go.usa.gov/xKQxB.

[55] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, DOE Announces $80

Million in Funding to Increase SuperTruck Efciency, March 2016. http://go.usa.gov/xBCvT.

[56] U.S. Department of Energy, Energy Information Administration, “Table 10.10: Advanced Metering Count

by Technology Type,” Electric Power Annual 2014, October 2015. http://go.usa.gov/3Snx4.

[57] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, DOE Previews Smart

Energy Analytics Campaign, May 2015. http://go.usa.gov/xBkDW.

[58] Smart Energy Analytics Campaign, Welcome to the Smart Energy Analytics Campaign, Accessed

September 2016. https://smart-energy-analytics.org/.

[59] Committee on the Assessment of Technologies for Improving Fuel Economy of Light-Duty Vehicles,

Phase 2; Board on Energy and Environmental Systems; Division on Engineering and Physical Sciences;

National Research Council; Cost, Effectiveness, and Deployment of Fuel Economy Technologies for

Light-Duty Vehicles, The National Academies Press, 2015. http://www.nap.edu/21744.

[60] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Lightweight Materials for

Cars and Trucks, Accessed September 2016. http://go.usa.gov/3SnrB.

[61] S. Wetzel, Casting of the Year: Magnesium Liftgate Cuts Weight, Adds Value, Modern Casting, May 2016.

http://www.afsinc.org/multimedia/contentMC.cfm?ItemNumber=19235.

References 23

[62] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Multi-Material

Lightweight Vehicle Helps Bring Technologies to Market, July 2016. http://go.usa.gov/xKevP.

[63] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Hydrogen and Fuel Cells

Program Record 15105, September 2015. http://go.usa.gov/xWkzx.

[64] U.S. Department of Energy, Ofce of Energy Efciency and Renewable Energy, Fuel Cell Technologies

Market Report 2015 (Draft), 2016. http://go.usa.gov/xBkMB.

[65] J. Voelcker, Mercedes-Benz GLC to offer world's rst plug-in fuel-cell powertrain, Green Car Reports,

June 2016. http://www.greencarreports.com/news/1104440_mercedes-benz-glc-to-offer-worlds-rst-plug-

in-fuel-cell-powertrain.

[66] R. Truett, GM to provide fuel cell vehicle to Army for testing, Automotive News, November 2015.

http://www.autonews.com/article/20151111/OEM05/151119956/gm-to-provide-fuel-cell-vehicle-to-

army-for-testing.

[67] H. Boeriu, BMW 5 Series GT Hydrogen Fuel Cell prototype spotted during testing, BMW Blog, August

2016. http://www.bmwblog.com/2016/08/09/bmw-5-series-gt-hydrogen-fuel-cell-prototype-spotted-

testing/.