U.S. DEPARTMENT OF ENERGY

Revolution…Now

The Future Arrives for Five Clean Energy

Technologies – 2015 Update

November 2015

ii

Contributors

Luke Bassett, DOE Office of Energy Policy & Systems Analysis and Office of

Energy Efficiency & Renewable Energy

James Brodrick, DOE Building Technologies Office

Steve Capanna, DOE Office of Energy Efficiency & Renewable Energy

Jonathan Castellano, DOE Vehicle Technologies Office

Christy Cooper, DOE Vehicle Technologies Office

Paul Donohoo-Vallett, DOE Office of Energy Efficiency & Renewable Energy

David Feldman, National Renewable Energy Laboratory

Roland Gravel, DOE Vehicle Technologies Office

Jason Hartke, DOE Building Technologies Office

David Howell, DOE Vehicle Technologies Office

Amy Jiron, DOE Building Technologies Office

Tarak Shah, DOE Office of the Under Secretary for Science and Energy

Gurpreet Singh, DOE Vehicle Technologies Office

Carol Schutte, DOE Vehicle Technologies Office

Rich Tusing, DOE Wind Technology Office

Jacob Ward, DOE Vehicle Technologies Office

Disclaimer: any mention of a specific company is not meant to imply an endorsement on the part of the U.S.

Department of Energy or U.S. Government.

iii

Contents

Expanding Scope ........................................................................................................................................ 1

Land-Based Wind Power ............................................................................................................................ 3

Big Fans of Wind Power ........................................................................................................................ 3

Wind in the Sales .................................................................................................................................... 4

Growing Up ............................................................................................................................................ 4

Solar PV: Utility-Scale ................................................................................................................................. 6

Stepping Out of the Shade ...................................................................................................................... 6

59% Cheaper .......................................................................................................................................... 6

How Low Can You Go? ......................................................................................................................... 7

A Solar Flare of Activity ........................................................................................................................ 8

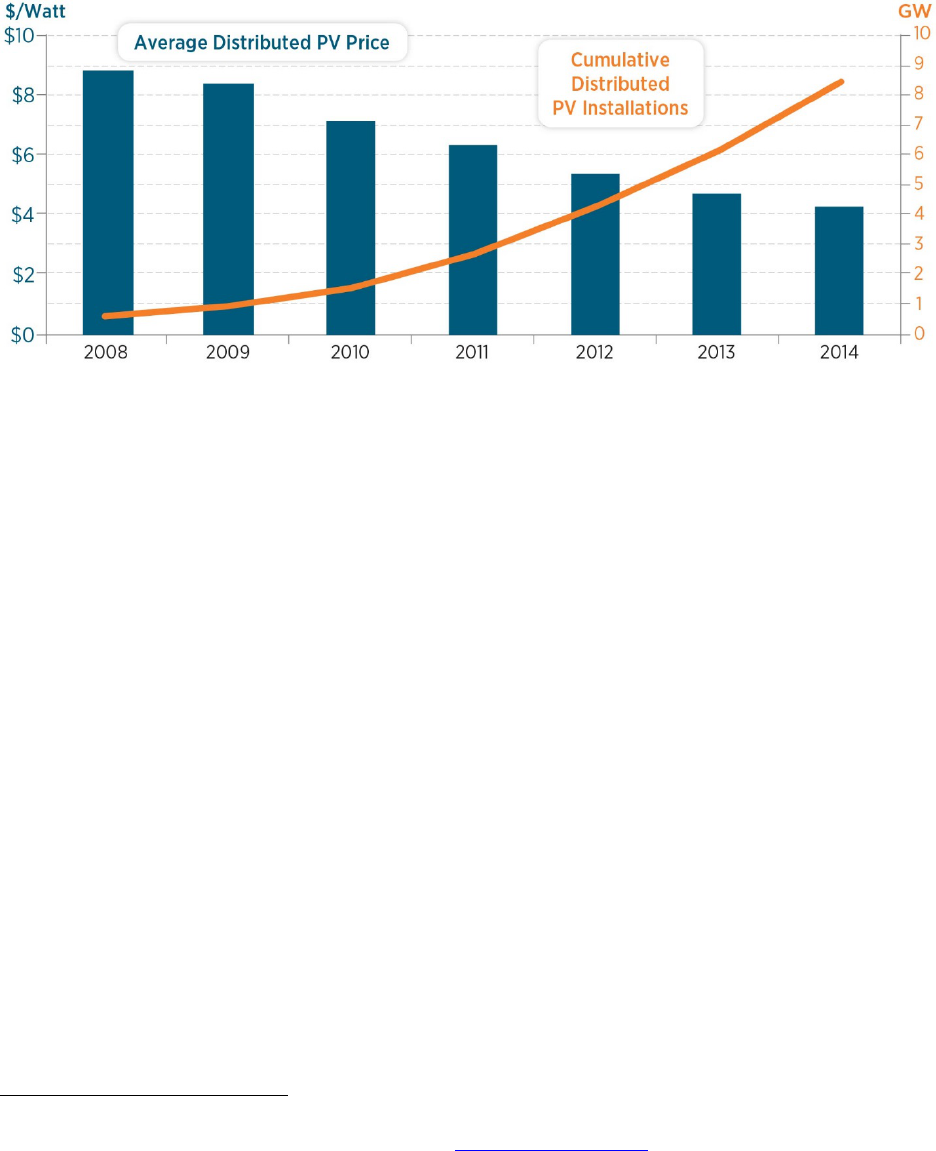

Solar PV: Distributed Generation .............................................................................................................. 9

Raise the Roof(top) ................................................................................................................................ 9

Soft Costs ............................................................................................................................................... 9

A Capital Idea ....................................................................................................................................... 10

Forecast: Sunny .................................................................................................................................... 10

LED Lighting .............................................................................................................................................. 11

Turning Up the Lights .......................................................................................................................... 11

Beyond the Bulb ................................................................................................................................... 12

A Bright Future .................................................................................................................................... 12

Electric Vehicles ........................................................................................................................................ 14

Putting it into High Gear ...................................................................................................................... 14

Charging Ahead with Batteries ............................................................................................................ 15

Road to the Future................................................................................................................................. 15

Revolution Next ......................................................................................................................................... 17

Sweet Suite of Smart Building Technologies ................................

....................................................... 18

Freight Trucks That Can Keep on Trucking ......................................................................................... 19

Vehicle Lightweighting: Lighten the Load and Hit the Road .............................................................. 20

Conclusion ................................................................................................................................................. 21

1

2

Expanding Scope

For decades, America has anticipated the transformational impact of clean energy technologies.

As the federal government and industry made long-term investments to support those

technologies, some critics became impatient, claiming a clean energy future would “always be

five years away.”

Today, the clean energy future has arrived.

In 2013, the U.S. Department of Energy (DOE) released the Revolution Now report, highlighting

four transformational technologies: land-based wind power, silicon photovoltaic (PV) solar

modules, light-emitting diodes (LEDs), and electric vehicles (EVs). That study and its 2014

update showed how dramatic reductions in cost are driving a surge in consumer, industrial, and

commercial adoption for these clean energy technologies—as well as yearly progress.

In addition to presenting the continued progress made over the last year in these areas, this year’s

update goes further. Two separate sections now cover large, central, utility-scale PV plants and

smaller, rooftop, distributed PV systems to highlight how both have achieved significant

deployment nationwide, and have done so through different innovations, such as easier access to

capital for utility-scale PV and reductions of non-hardware costs and third-party ownership for

distributed PV.

Along with these core technologies, this update briefly introduces three additional technologies

on the cusp of wider deployment and cost reduction in the coming years: smart building systems,

fuel-efficient freight trucks, and vehicle lightweighting.

Today, clean energy technologies are providing real-world solutions—not only do they reduce

the carbon pollution that causes climate change, but they also drive a domestic energy economy

with technologies that are increasingly cost-competitive with existing conventional technologies,

even without accounting for the climate benefits. Clean energy manufacturing and installations

have also become major opportunities for American workers in the 21

st

century.

Even though we are seeing the results of the enormous progress these technologies have

achieved, there is still more that can be accomplished. DOE’s recent Quadrennial Technology

Review identified hundreds of clean energy research and innovation opportunities in our homes,

businesses, cars and trucks, and in the power sector, that with sustained investment will provide

real-world solutions to our energy challenges.

1

With the continued progress of the core technologies in this report, and more innovations on the

horizon, the clean energy revolution is clearly transforming the way we produce and use energy.

1

Found at http://energy.gov/qtr.

3

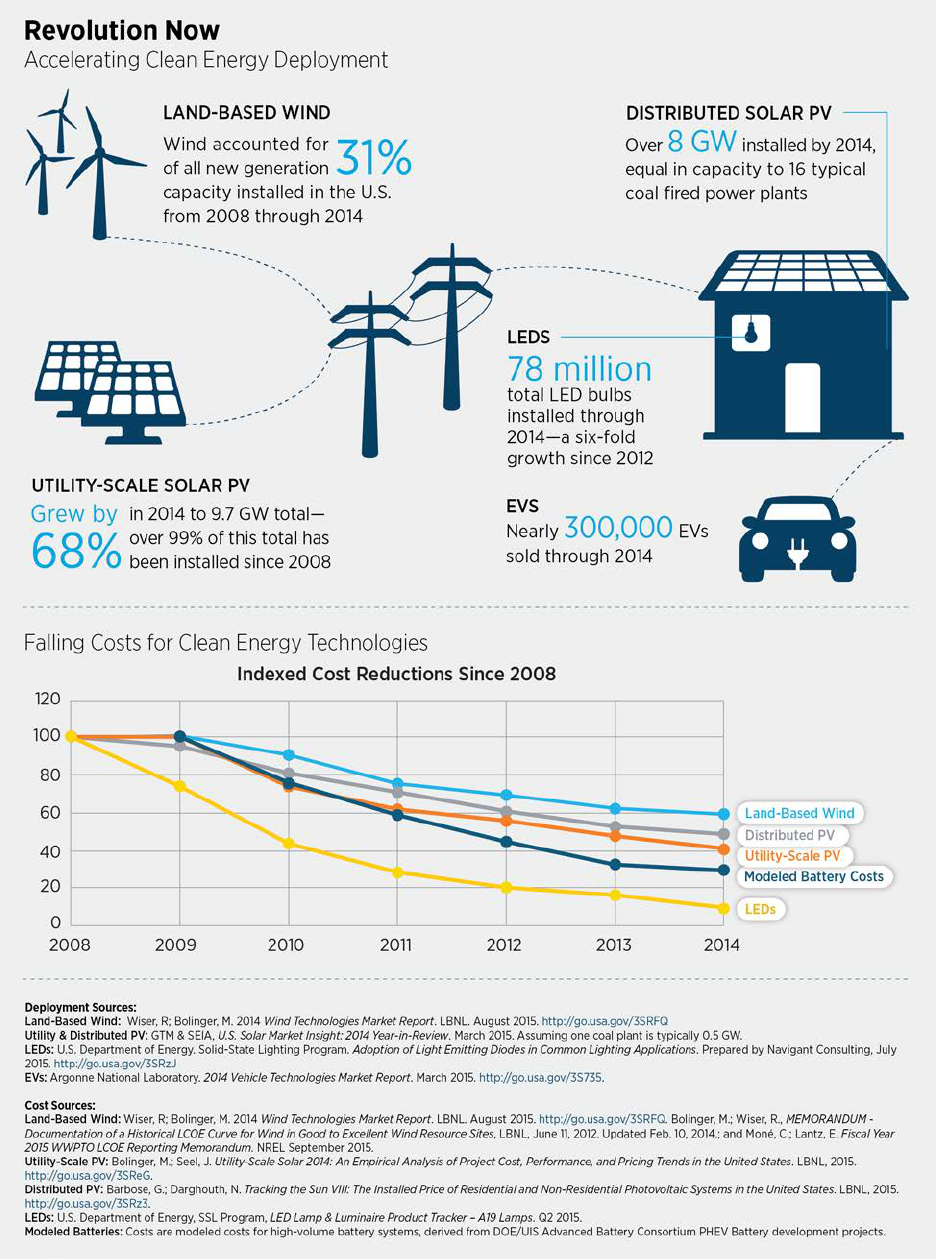

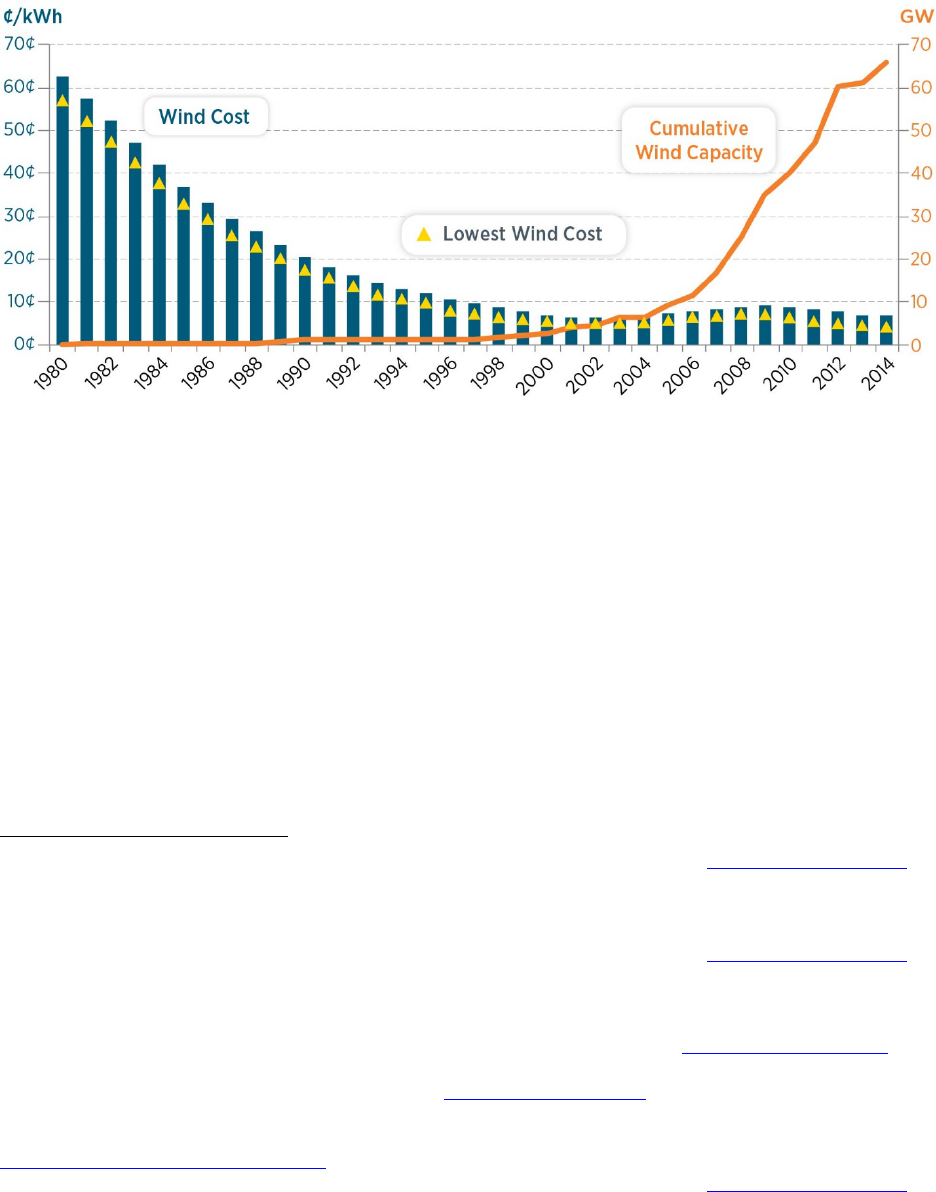

Land-Based Wind Power

Notes: 1 gigawatt (GW) = 1,000 megawatts (MW). All costs shown are inflation adjusted to dollar year 2014 and

exclude the production tax credit (PTC). Wind capacity as reported by market reports.

2

“Wind Cost” represents

estimated levelized cost of energy from a representative wind site, and “Lowest Wind Cost” represents costs derived

from power purchase agreements from good to excellent wind resource sites in the interior of the country.

3

Big Fans of Wind Power

Wind power is firmly entrenched as a mainstream power source: between 2008 and 2014, wind

power accounted for 31% of all new generation capacity added in the United States.

4

As of 2014,

there were more than 65,000 megawatts (MW) of utility-scale wind power deployed across 39

states

5

—enough to generate electricity for more than 16 million households

6

—with another

13,600 MW under construction as of the first quarter of 2015.

7

Wind now provides 4.4% of total

U.S. electricity generation, 23 states have at least 500 MW of wind installed, and in nine states,

wind exceeds 10% of total in-state electricity generation.

8,9

This ramp up in generation has

yielded enormous benefits: wind power in the United States in 2013 reduced annual carbon

dioxide emissions by more than 115 million metric tons and reduced water consumption by more

2

Wiser, R; Bolinger, M. 2014 Wind Technologies Market Report. LBNL. August 2015. http://go.usa.gov/3SRFQ.

3

Ibid; Bolinger, M.; Wiser, R., MEMORANDUM - Documentation of a Historical LCOE Curve for Wind in Good to

Excellent Wind Resource Sites, LBNL, June 11, 2012. Updated Feb. 10, 2014.; and Moné, C.; Lantz, E. Fiscal Year

2015 WWPTO LCOE Reporting Memorandum. NREL September 2015.

4

Wiser, R; Bolinger, M. 2014 Wind Technologies Market Report. LBNL. August 2015. http://go.usa.gov/3SRFQ.

Note that this report has an error and incorrectly states this number as 33%.

5

Ibid.

6

Wind generated 181,791 GWh in 2014 (Energy Information Administration, Electric Power Monthly, “Table

1.1.A. Net Generation from Renewable Sources: Total (All Sectors).” October 2015. http://go.usa.gov/cYAZm

). The

average American household consumed 10,932 kWh in 2014 (Energy Information Administration. How much

electricity does an American home use? October 2015.

http://go.usa.gov/cYAKh).

7

American Wind Energy Association. AWEA U.S. Wind Industry First Quarter 2015 Market Report. April 2015.

8

Energy Information Administration. Electric Power Monthly – Detailed State Data.

http://www.eia.gov/electricity/data/state/

. Accessed October 2015.

9

Wiser, R; Bolinger, M. 2014 Wind Technologies Market Report. LBNL, August 2015. http://go.usa.gov/3SRFQ.

4

than 36 billion gallons, all while supporting more than 50,000 U.S. manufacturing, construction,

and wind operations jobs.

10

Wind in the Sales

This success has been enabled in part due to recent reductions in the cost of wind power as U.S.

wind power prices have reached an all-time low. Power purchase agreements for wind have

fallen from rates up to 7 cents/kilowatt-hour (kWh) in 2009 to an average of 2.4 cents/kWh in

2014.

11

This low-cost wind power arises from projects installed in excellent resource locations in

the central part of the country and is reflective in part of the federal production tax credit (PTC).

This significant reduction in cost in only five years is a result of multiple factors. First, DOE’s

sustained investment in improving wind technology, with $2.4 billion dollars invested in wind

research and development between 1976 and 2014, has honed the technology and enabled many

key improvements such as the taller turbines and longer blades highlighted below.

12

Additionally, new transmission projects, such as those in the recently completed Texas

Competitive Renewable Energy Zone transmission build-out, have enabled wind development in

more areas of the country. Recent expanded coordination among grid operators has increased the

ability of the grid to accept higher levels of wind generation while reducing curtailment.

13

State

renewable portfolio standards and federal PTC policies have assisted deployment of continued

investment in U.S. wind manufacturing.

Together, these investments, infrastructure projects, and policies have made wind a low-cost,

zero-carbon alternative that contributes to the transformation of the U.S. electricity generation

portfolio.

Growing Up

Continued innovation in next generation wind technologies could soon enable cost-competitive

wind potential nationwide. One of the biggest changes in recent years is that wind turbines

themselves are getting bigger: a wind turbine installed today on average has 108% longer blades

and is 48% taller than one installed in 1999.

14

Taller turbines and longer blades allow access to

the stronger and more consistent wind speeds that occur at higher altitudes, produce more

electricity per tower thus minimizing the land area needed, and enable more cost-effective wind

power. DOE estimates that the continued development of taller wind towers coupled with larger

rotors and advanced turbine designs would grow wind’s potential electrical output by 67% above

10

U.S. Department of Energy. “Chapter 2 – Wind Power in the United States.” Wind Vision. March 2015.

http://go.usa.gov/crxhR

.

11

Wiser, R; Bolinger, M. 2014 Wind Technologies Market Report. LBNL. August 2015. http://go.usa.gov/3SRFQ.

Note that these prices include the effect of the federal PTC and as such are lower than what is displayed in the chart

above.

12

Inflation adjusted to 2014 dollars using U.S. Bureau of Economic Analysis GDP budget deflator. 1978-2008:

Pelsoci, T.; Retrospective Benefit-Cost Evaluation of U.S. DOE Wind Energy R&D Program. June 2010.

http://go.usa.gov/3SRFY

. 2009-2014: DOE Office of Energy Efficiency and Renewable Energy budget justification

documents at http://go.usa.gov/3SRMx.

13

Wiser, R; Bolinger, M. 2014 Wind Technologies Market Report. LBNL. August 2015. http://go.usa.gov/3SRFQ.

14

Ibid.

5

the wind technologies currently deployed, opening up an additional 700,000 square miles—or

about one-fifth of the United States—for wind development.

15

This expansion of potential wind

generation also occurs in much of the Southeastern portion of the country, an area that has

historically not seen significant wind development.

In addition to these technological innovations, investments in supercomputing power are further

optimizing whole wind plants and unlocking future cost reductions and efficiency improvements.

Advanced computational modeling of the complex wind interactions across turbines coupled

with improved sensing, advanced controls, and wind forecasting will increase efficiency and

reliability to create the next generation of wind power technologies.

In many parts of the country, wind power is already becoming a cost-effective low carbon

solution that supports U.S. jobs in manufacturing and construction—but wind still has large

additional untapped potential, as shown in a recent DOE report which outlined how wind could

generate 20% of the nation’s electricity by 2030.

16

With ongoing technological innovation,

transmission expansion, and continued federal and state support, wind can continue to grow and

unlock its wide array of benefits in all 50 states.

15

U.S. Department of Energy. Enabling Wind Power Nationwide. May 2015. http://go.usa.gov/3SRMj.

16

U.S. Department of Energy. Wind Vision. March 2015. http://energy.gov/eere/wind/wind-vision.

6

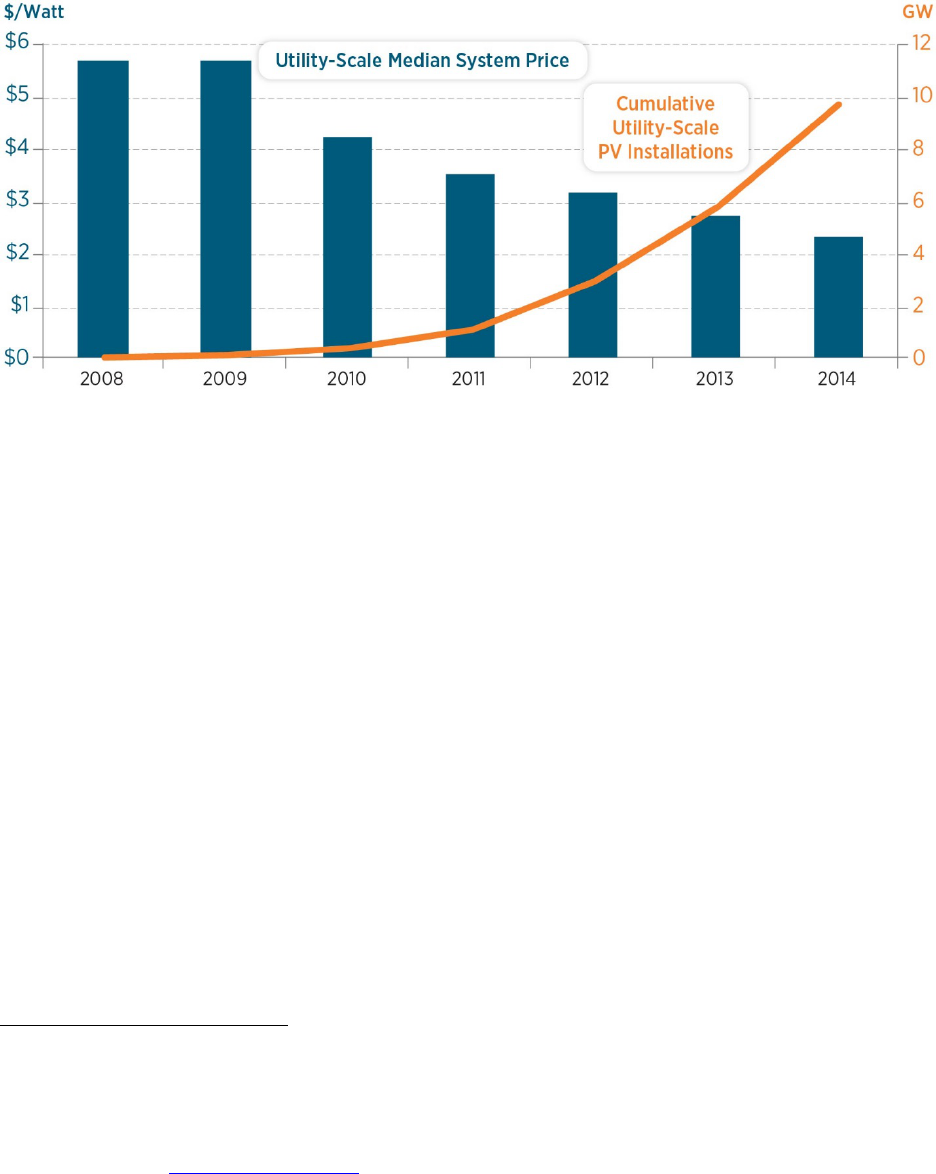

Solar PV: Utility-Scale

Notes: All prices are in $/W

DC

and inflation adjusted to dollar year 2014. 1 gigawatt (GW) = 1,000 megawatts (MW).

Prices as reported in market report.

17

“Utility-scale” cumulative installations as reported in source in GW

DC

.

18

Stepping Out of the Shade

Although the energy potential of the sun is limitless for practical purposes, the cost of converting

that energy into usable electricity has long kept solar PV out of reach for all but a few niche

applications. However, over the last several years, thanks to cost declines and technological

advances, solar PV went from a novelty to a large-scale generation source purchased by electric

utilities to meet demand.

Utility-scale PV has rapidly emerged as a mainstream technology over the last few years. By

2014, the total capacity of large utility-scale solar PV reached 9.7 GW with over 99% of these

installations occurring after 2008.

19

This trend has continued with 15% of all electric generating

capacity brought online from January to September 2015 arising from utility-scale PV

.

20

59% Cheaper

This large deployment is a result of the dramatic decline in the price of PV systems. Between

2008 and 2014, the cost for a PV module declined from $3.57/watt (W) to about $0.71/W.

21

Total cost declines mirrored this hardware cost reduction due to improvements in installation and

business practices: the total cost of utility-scale PV systems fell from $5.70/W in 2008 to

17

Bolinger, M.; Seel, J. Utility

‐

Scale Solar 2014: An Empirical Analysis of Project Cost, Performance, and Pricing

Trends in the United States. LBNL, September 2015. http://go.usa.gov/cYAp4.

18

GTM & SEIA, U.S. Solar Market Insight: 2014 Year-in-Review. March 2015.

19

Ibid.

20

Federal Energy Regulatory Commission, Office of Energy Projects, Energy Infrastructure Update for September

2015. October 2015. http://go.usa.gov/craZB

.

21

Mints, P., Photovoltaic Manufacturer Shipments: Capacity, Price & Revenues 2014/2015. SPV Market Research.

April 2015.

7

$2.34/W in 2014—a decrease of 59%.

22

This means solar is increasingly reaching cost parity

with traditional electrical generation from natural gas and coal in parts of the United States.

A combination of DOE, federal, state, and industry actions helped achieve this drastic cost

reduction in a short period of time. DOE’s $4.1 billion investment in PV technology research and

development (R&D) from 1975 through 2008 accelerated the cost reduction progress by an

estimated 12 years, while providing a net economic benefit of $16.5 billion.

23

The federal

Investment Tax Credit (ITC) along with state renewable portfolio standards and other state and

local incentives for PV in the United States—as well as the European Union members, Japan,

China, and other countries—have also effected solar deployment, further reducing manufacturing

costs.

How Low Can You Go?

In 2014 and 2015, several PV system installers won power purchase contracts over traditional

sources of generation and signed power purchase agreements with utilities to provide electricity

at a cost between 4 to 5 cents/kWh. These are not just simple one-off projects with unusually

good economics; utilities have on multiple occasions received proposed projects in this price

range with aggregate capacity of more than 10 times the capacity requested.

24

Even though those

prices are enabled by the federal tax credit, they represent a price offering that would have

seemed shockingly low just a few years ago.

The utility-scale PV industry was, in part, kick-started by DOE’s Loan Programs Office (LPO).

Through funding provided by the Recovery and Reinvestment Act of 2009, the LPO financed the

first five utility-scale solar PV projects over 100 MW in the United States with more than 1,500

MW of total capacity. Today, utility-scale solar is being financed by the private sector at

increasing scale. As of summer 2015, there were 21 privately financed utility-scale solar PV

projects over 100 MW either built or under construction.

25,26

These low prices are also a result of new types of financial instruments specifically for clean

energy projects like utility-scale solar PV, which provide a low cost source of capital. For

example, as of mid-2015, six specially structured publicly traded companies had financed

approximately 4,500 MW of solar, offering dividend yields between 3% and 7%.

27

As a

testament to solar’s technological progress, enormous potential, and overall maturity of the

industry, large financial institutions now view utility-scale solar PV as an attractive investment.

22

Bolinger, M.; Seel, J. Utility

‐

Scale Solar 2014: An Empirical Analysis of Project Cost, Performance, and Pricing

Trends in the United States. LBNL, September 2015. http://go.usa.gov/cYAp4.

23

“Retrospective Benefit-Cost Evaluation of DOE Investment in Photovoltaic Energy Systems.” DOE, August

2010. http://go.usa.gov/3SRMh

. Inflation adjusted to 2014 dollars using U.S. Bureau of Economic Analysis GDP

budget deflator.

24

Bolinger, M.; Seel, J. Utility

‐

Scale Solar 2014: An Empirical Analysis of Project Cost, Performance, and Pricing

Trends in the United States. LBNL, September 2015. http://go.usa.gov/cYAp4.

25

U.S. Department of Energy, Loan Programs Office. Powering New Markets: Utility-Scale Photovoltaic Solar.

February 2015. http://go.usa.gov/3SRez

.

26

SEIA. “Major Solar Projects in the United States: Operating, Under Construction, or Under Development.”

Updated Aug. 20, 2015.

27

Based on internal NREL analysis of the market and yieldco investor presentations from the first half of 2015.

8

A Solar Flare of Activity

As of mid-2015, there were more than 27,000 MW of utility-scale solar projects under

development, with 3,600 MW already under construction.

28

Even if only a portion of these

projects are built, it will easily double existing capacity over the next few years. This large

pipeline of planned projects is partially due to the pending expiration of the ITC at the end of

2016, which has allowed the industry to flourish by providing clear, long-term policy certainty.

29

So, as with wind, sustained federal and state support can help continue this rapid pace of utility-

scale solar deployment beyond the next few years.

In the longer term, the potential for solar to eventually provide a much larger share of our

electricity portfolio is dramatic: enough solar resource and land area is available for utility-scale

PV to generate over 69 times the electricity needs of the nation.

30

With the help of additional

investments and innovations in inverters, electricity storage, advanced materials, and new

electricity market structures, more of this potential of clean energy could be unlocked.

31

The

recent burst of activity in this sector has exceeded expectations, but for the future of utility-scale

PV the sky really is the limit.

28

SEIA. Major Solar Projects in the United States: Operating, Under Construction, or Under Development.

Updated Aug. 20, 2015.

29

Deutsche Bank Group, Paying for Renewable Energy: TLC at the Right Price. DB Climate Change Advisors.

December 2009.

30

Utility PV technical potential 282,800 TWh (Lopez, A; Roberts, B.; Heimiller, D.; Blair, N.; and Porro, G; U.S.

Renewable Energy Technical Potentials: A GIS-Based Analysis. NREL. July 2012. http://go.usa.gov/3SRtC

). Total

2014 U.S. electricity generation 4,093 TWh (Energy Information Administration, Electric Power Monthly, “Table

1.1. Net Generation by Energy Source: Total (All Sectors),” October 2015.

http://go.usa.gov/cYF5P).

31

U.S. Department of Energy. Quadrennial Technology Review. Chapter 4, “Advancing Clean Electric Power

Technologies,” September 2015. http://energy.gov/qtr

.

9

Solar PV: Distributed Generation

Notes: All prices are in $/W

DC

and inflation adjusted to dollar year 2014. 1 gigawatt (GW) = 1,000 megawatts (MW).

Capacity weighted average as reported by market report for residential systems only.

32

Non-residential systems are

typically larger and have lower reported prices. Capacity is cumulative distributed residential and non-residential

capacity, in GW

DC

.

33

Raise the Roof(top)

Distributed PV systems use the same basic PV technology as larger utility-scale projects, but

they differ in one key aspect: they are located where the electricity is used. These systems are

often on individual consumers’ rooftops and are frequently not owned by a power company. This

is unlike the vast majority of electricity generation facilities, where a power company generates

electricity at a central plant and then sends it to consumers via the electric grid.

Although distributed PV technology has been available for years, falling prices over the last

decade have unlocked its potential not only for the average homeowner but also for larger

consumers like businesses and schools. Many installations are small enough to fit on a roof, but

there is nothing tiny about distributed PV’s growth. As of the summer of 2015, there have been

nearly 800,000 cumulative distributed PV installations. This represents almost 10,000 MW in

capacity, which is nearly equal to the capacity of utility-scale installations.

34

Soft Costs

The cost of solar energy system hardware (i.e., panels, inverters, etc.) has dropped significantly,

but the non-hardware “soft” costs of solar—such as permitting, installation, interconnection, and

maintenance fees—remain a major barrier to greater deployment nationwide and can account for

up to 68% of total system costs.

35

To address this problem, DOE launched the Rooftop Solar

Challenge in 2011 to slash red tape and make installing rooftop solar PV easier, faster, and more

affordable, and the on going Race to 7-Day Solar prize competition continues to drive innovation

32

Barbose, G.; Darghouth, N. Tracking the Sun VIII: The Installed Price of Residential and Non-Residential

Photovoltaic Systems in the United States. LBNL, 2015. http://go.usa.gov/3SRz3

.

33

GTM & SEIA, U.S. Solar Market Insight: 2014 Year-in-Review. March 2015.

34

GTM & SEIA. U.S. Solar Market Insight Report: Q2 2015. September 2015.

35

GTM & SEIA. U.S. Solar Market Insight Report: Q3 2014. November 2014.

10

in this area. Efforts such as these appear to be turning the tide; even though module costs have

been relatively constant since 2012, distributed PV prices have continued to drop, indicating that

soft costs have been the major source of price reductions for the last two years.

36

Although these recent declines in soft costs have been impressive, this area continues to hold the

greatest potential for future cost reductions. For example, specific cities with the most favorable

PV permitting processes were found to have prices up to 12% lower than the median state-wide

price.

37

Similarly in 2014, despite comparable hardware costs, residential system pricing in

Germany was reported to be $2.13/W compared to $4.17/W in the United States.

38

These

examples indicate the huge potential to make further soft cost reductions.

A Capital Idea

Years ago, consumers had only one option if they wanted to install PV on their homes: pay for

the whole system upfront and wait for savings to accrue over time. This created a major barrier,

as most consumers could not afford the upfront costs, even if they would actually end up saving

money over the life of the system. However, consumers today have many new options available

to them. Third-party-ownership of PV systems has revolutionized the distributed PV market.

Similar to leasing a car, third-party ownership allows consumers to benefit from lower electricity

payments without purchasing the whole PV system directly. The success of this model has been

clear—third-party financing accounted for more than 72% of U.S. residential PV systems

installed in 2014.

39

In addition, other business and financing innovations such as zero-down solar loans, shared

community solar, and property assessed clean energy financing (also called PACE) are making it

much easier and more affordable for consumers to install rooftop PV.

Forecast: Sunny

The cost reduction and deployment growth of distributed PV is expected to continue, as experts

project the installed prices of residential PV systems to fall an additional 16-33% by 2020.

40

An

August 2015 DOE LPO announcement provided guidance on how distributed energy projects

may be eligible for DOE loan guarantees; those loan guarantees, along with other policy support,

could enable innovative technology solutions to overcome remaining market barriers and deliver

clean, cost-competitive distributed solar energy right to consumers’ doorsteps in virtually every

state in the nation.

41

36

Barbose, G.; Darghouth, N. Tracking the Sun VIII: The Installed Price of Residential and Non-Residential

Photovoltaic Systems in the United States. LBNL, 2015. http://go.usa.gov/3SRz3

.

37

Wiser, R.; Dong, C. The Impact of City-level Permitting Processes on Residential Photovoltaic Installation Prices

and Development Times. LBNL, 2013. http://go.usa.gov/3SRtF

.

38

Barbose, G.; Darghouth, N. Tracking the Sun VIII: The Installed Price of Residential and Non-Residential

Photovoltaic Systems in the United States. LBNL, 2015. http://go.usa.gov/3SRz3

.

39

GTM Research (2015). U.S. Residential Solar Financing 2015-2020.

40

Feldman, et. al. Photovoltaic System Pricing Trends: Historical, Recent, and Near

‐

Term Projections - 2015

Edition. LBNL and NREL. August 2015. http://go.usa.gov/3SRMH

.

41

U.S. Department of Energy, Loan Programs Office. Distributed Energy Projects. Accessed September 2015.

http://go.usa.gov/3SRz9

.

11

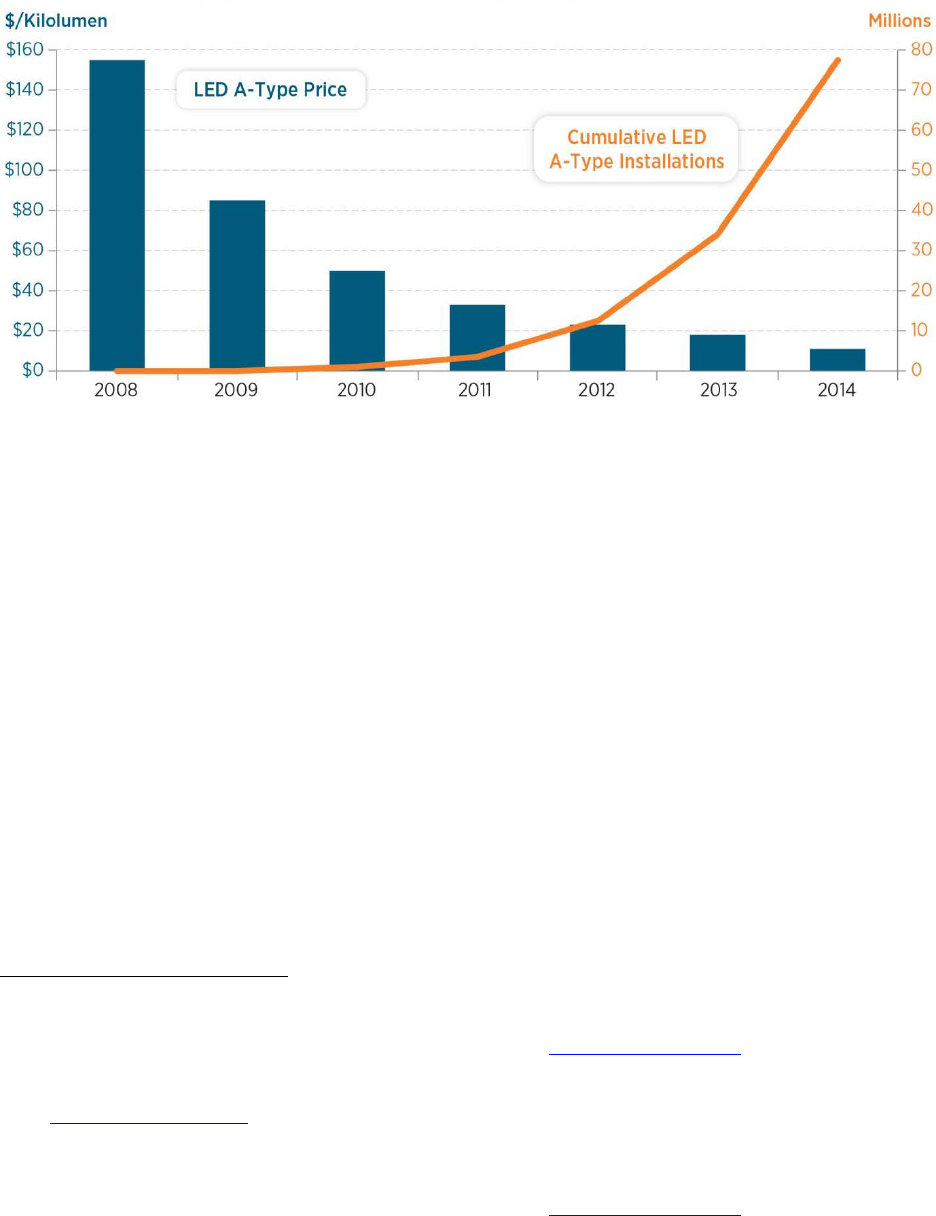

LED Lighting

Notes: Kilolumen is a measure of visible light output by a source. Price data is in nominal dollars as reported in

internal tracking report.

42

Cumulative LED A-type bulb installations as reported in market report.

43

Turning Up the Lights

Stand underneath a traditional incandescent bulb and a LED bulb

44

and you will soon feel the

difference between the two— heat. While both produce the same amount of light, the

incandescent bulb is too hot to touch, a clear sign that much of the energy it uses is being wasted.

LED technologies have cut this wasted energy out of lighting: the best performing 60 W

equivalent LED bulbs available now consume 85% less energy than incandescent bulbs.

45

LEDs

are spurring a dramatic change in lighting due to their vast energy savings potential, lower costs,

improved performance, and added benefits like long lifetime and maintenance savings.

These benefits are moving LEDs into the mainstream. From 2012 to 2014, total installations of

common home LED bulbs increased six-fold from 13 million to 78 million—particularly rapid

growth considering there were fewer than 400,000 installations as recently as 2009. LED bulbs

now account for 2.4% of all currently installed lighting of this type – growth enabled by the

nearly 90% reduction in cost since 2008.

46

This success is a direct result of government-industry R&D investments to bring down costs,

improve efficiency and performance, and foster domestic manufacturing of LED lighting

42

U.S. Department of Energy, SSL Program, LED Lamp & Luminaire Product Tracker – A19 Lamps. Q2 2015.

43

U.S. Department of Energy. Solid-State Lighting Program. Adoption of Light Emitting Diodes in Common

Lighting Applications. Prepared by Navigant Consulting, July 2015. http://go.usa.gov/3SRzJ

.

44

In this report, “LED bulbs” refers to A-Type bulbs that are common in household applications.

45

Calculated from U.S. Department of Energy. LED Lighting Facts – CALiPER Snapshot “Light Bulbs”, October

2013. http://go.usa.gov/3SRzA

. See page 3, note 6. The best performing LED bulb approaches 90 lumens/W

efficacy. To produce 800 lumens this LED draws 8.89 W of power, a 85% reduction compared to the 60 W of power

drawn by the equivalent incandescent bulb.

46

U.S. Department of Energy. Solid-State Lighting Program. Adoption of Light Emitting Diodes in Common

Lighting Applications. Prepared by Navigant Consulting, July 2015. http://go.usa.gov/3SRzJ

.

12

components and products. In the past decade, modest yet highly strategic investments by DOE

have helped to make the United States the hub of LED lighting innovation. Today, America is

beginning to reap the rewards of these years of investment. Looking at the bigger picture across

all LED product types, LED installations prevented 7.1 million metric tons of CO

2

emissions and

saved $1.4 billion in energy costs in 2014 alone.

47

Beyond the Bulb

DOE and many in the lighting industry are looking toward the potential energy savings in the

commercial and industrial sectors offered by replacing fluorescent overhead lighting common in

most offices and manufacturing facilities. Energy impacts in these applications are

disproportionally high relative to market share because of the large number of installations and

extended operating hours. In contrast to lighting in homes, which average less than two hours of

operation per day, commercial and industrial lighting fixtures average about 12 hours of

operation per day.

Achieving the greatest possible market adoption and energy savings from LED products will

require ongoing technology R&D improvements. Unlike conventional lighting sources, LED

technology has significant headroom for additional technology advancements and DOE is

working with industry to continue to reduce costs through improved materials and optics,

optimized product design and assembly, boosting lumen outputs, and integrating LEDs with

lighting control systems, which will enable even greater energy savings. DOE analysis has

shown that with aggressive research and development, LED product efficiency can still be

almost doubled, from the current 125-135 lumens per watt to 230 lumens per watt.

48

A Bright Future

Fully capitalizing on the promise of LED technology will catapult our nation forward in creating

a clean energy future. Energy-efficient technologies like LED lighting not only reduce the

consumption of fossil fuels, they go hand-in-hand with making renewable energy more

competitive. For example, further cost reductions in LED lighting will make it far more

affordable and practical to construct zero-energy buildings—buildings so energy efficient that

renewable energy systems can offset all or most of their annual energy consumption. Likewise,

the conversion to LED street lighting will enable cities and towns across the country to

dramatically reduce their energy and maintenance costs.

LEDs are projected to reach over 80% of all lighting sales by 2030 driven by performance

increases and cost savings relative to conventional lighting.

49

This would save Americans $26

47

U.S. Department of Energy. Solid-State Lighting Program. Adoption of Light Emitting Diodes in Common

Lighting Applications. Prepared by Navigant Consulting, July 2015. http://go.usa.gov/3SRzJ

. Emission savings

calculated by converting the reported 143 trillion BTU of source energy savings to site energy using a 3.05 site-to-

source ratio, converting to electricity savings using 3412 BTU/kWh, and multiplying by the national CO

2

emission

intensity of 1,136 lbs CO

2

/MWh as reported by eGRID 2012 (http://go.usa.gov/crX6e).

48

Efficiency (luminaire efficacy) is projected to reach 196 lumens/W in 2020. U.S. Department of Energy. Solid-

State Lighting Program. Solid State Lighting R&D Plan. May 2015. http://go.usa.gov/cr4Sh

.

49

U.S. Department of Energy. Solid State Lighting Program. Energy Savings Forecast of Solid-State Lighting in

General Illumination Applications. Prepared by Navigant Consulting, August 2014. http://go.usa.gov/3SRuB

.

13

billion per year in electricity costs,

50

while cutting America’s lighting electricity use by nearly

half.

51

Developing this technology domestically also allows American manufacturing to benefit

from exporting LEDs to rapidly electrifying developing nations while enabling those countries to

save money and cut emissions by leapfrogging over less efficient lighting technologies.

50

Calculated from: 261 TWh projected electricity savings from LEDs in 2030 (Ibid). Average retail electricity price

for 2014 of 10.1 cents/kWh for residential, commercial, and industrial sectors (U.S. Department of Energy, Energy

Information Administration. Electric Power Monthly. “Table 5.3. Average Price of Electricity to Ultimate

Customers” Accessed October 2015. http://go.usa.gov/cYMpk

).

51

U.S. Department of Energy. Solid State Lighting Program. Energy Savings Forecast of Solid-State Lighting in

General Illumination Applications. Prepared by Navigant Consulting, August 2014. http://go.usa.gov/3SRuB

.

14

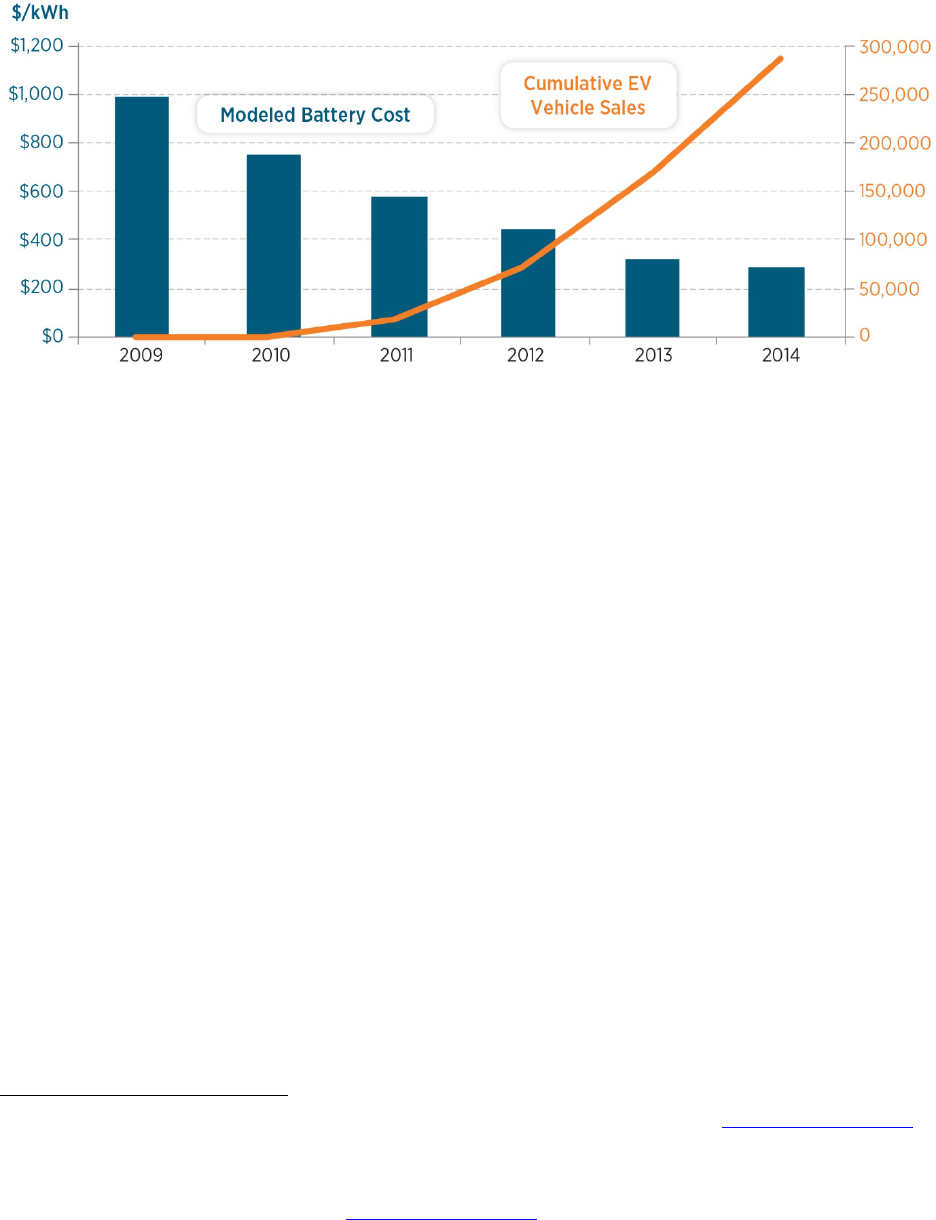

Electric Vehicles

Notes: Costs are modeled costs for high-volume battery systems, derived from DOE/UIS Advanced Battery

Consortium PHEV Battery development projects and are representative of nominal dollars. Sales as reported by

market tracker, here “EVs” include all plug-in hybrid and battery plug-in vehicles.

52

Putting it into High Gear

Americans bought nearly 120,000 electric vehicles (EVs)

in 2014, more than double the number

purchased in 2012. This brings the total number of EVs on U.S. roads to nearly 300,000 by the

end of 2014.

53

Today, EVs are supporting America’s energy and climate goals and helping

domestic manufacturing remain globally competitive in the 21

st

century.

This is good news for our climate, our health, and our economy. With zero tailpipe emissions,

EVs reduce local air pollution and help us breathe a little easier. They also enhance our energy

security by reducing our oil use, while substantially cutting carbon emissions. For example a

representative EV reduces greenhouse gas emissions by 48%, compared to a gasoline fueled

car.

54

EVs also will become cleaner over time as the nation’s electricity supply continues to move to

lower-emitting energy sources.

This continued growth is the direct result of combined federal, state, and industry efforts to

bring down the cost of EVs through research and development of better batteries, promoting

consumer adoption through tax and other incentives, and supporting public and private

investments in domestic EV manufacturing capacity. DOE’s utility partnership agreement with

Edison Electric Institute is intended to pick up this pace by collaborating with 70 utilities to

accelerate EV and charging infrastructure deployment. Continued collaboration and investment

in public education and outreach initiatives along with industry, state and federal support build

on these successes to ensure the continued increase in EV adoption.

52

Argonne National Laboratory. 2014 Vehicle Technologies Market Report. March 2015. http://go.usa.gov/3S735.

53

Ibid.

54

EV emissions are highly sensitive to geographic location; this number is based on the national electricity

generation fuel mix: U.S. Department of Energy, Alternative Fuels Data Center. Emissions from Hybrid and Plug-In

Electric Vehicles. Accessed October 2015. http://go.usa.gov/3Snq9

.

15

Charging Ahead with Batteries

The increase in EV sales in recent years has been enabled by the development of lower-cost

lithium-ion batteries supported by DOE research, which will continue to be a critical area going

forward. DOE models for EV battery fabrication costs have indicated that the expected cost of

EV batteries at high-volume has fallen by an astounding 70% since 2008.

55

The cost and performance of batteries are a key factor in continuing to lower the costs of EV

ownership. In addition to universities and industry, DOE has been a leader in battery R&D

investment: between 1992 and 2012, DOE invested $1 billion dollars in battery R&D, which

advanced the state-of-the-art by six years and created $3.5 billion worth of economic value.

56

This investment continues to pay off as rapidly falling costs mean that near-future battery costs

may be as low as $200/kWh by 2020.

57

Looking ahead, DOE is working with industry,

academia, and its national laboratories toward achieving an even more aggressive goal of

$125/kWh modeled production costs by 2022.

58

We can now see firsthand the results of advanced research in EV batteries making their way into

the market. For example, the energy storage capacity of the second-generation Chevrolet Volt

battery increased by 15% compared to the previous generation.

59

In general, optimization of cell

chemistry, design, and performance decrease the mass of battery packs, allowing EVs to travel

farther with full performance.

Road to the Future

Automakers are taking advantage of these innovations to design lower-priced EVs that are

poised to be strong competitors. For example, multiple automakers plan on delivering 200-mile-

range EVs for less than $40,000 around 2017.

60

As EVs accounted for 1.6% of all passenger cars

sold in 2014,

61

the potential for the next generation of EVs to impact transportation is large.

Improved charging infrastructure will also maintain momentum for EVs. There are now more

than 30,000 public and private EV charging outlets in the United States,

62

and as of August 2015,

55

Modeled costs are validated through applied research, and represent calculated high-volume commercial

production costs, rather than market price.

56

Inflation adjusted to 2014 dollars using U.S. Bureau of Economic Analysis GDP budget deflator. U.S. Department

of Energy. Benefit-Cost Evaluation of U.S. DOE Investment in Energy Storage Technologies for Hybrid and Electric

Cars and Trucks. Prepared by STI International. December 2013. http://go.usa.gov/3SnqJ

.

57

Nilson, M.; Nykvist, B.; Rapidly Falling Costs of Battery Packs for Electric Vehicles. Nature Climate Change,

April 2015. http://dx.doi.org/10.1038/nclimate2564

.

58

U.S. Department of Energy. EV Everywhere Grand Challenge. January 2014. http://go.usa.gov/3Sn3B.

59

“Chevrolet Introduces All-New 2016 Volt,” General Motors, January 12, 2015. Accessed Aug. 25, 2015:

http://media.gm.com/media/us/en/gm/news.detail.html/content/Pages/news/us/en/2015/Jan/naias/chevrolet/volt/0112

-volt-2016-intro.html.

60

Davies, A. “Chevy Could Beat Tesla to Building the First Mainstream Electric Car,” Wired. Accessed Aug. 21,

2015: http://www.wired.com/2015/01/chevrolet-bolt-ev

.

61

118,882 EVs sold in 2014 (Argonne National Laboratory. 2014 Vehicle Technologies Market Report. March

2015. http://go.usa.gov/3S735

) compared to 7,687,619 total passenger cars sold in 2014 (Ward’s Auto U.S. Car and

Truck Sales, 1931-2014. January 2015. http://wardsauto.com/keydata/historical/UsaSa01summary).

62

U.S. Department of Energy, Alternative Fuels Data Center. “Alternative Fueling Station Counts by State,”

Accessed October 2015. http://go.usa.gov/3S7rh

. Residential EVSE locations or “wall outlets” are not included.

16

the DOE Workplace Charging Challenge had partnered with more than 230 organizations that

have committed to providing EV charging for employees, increasing range confidence for

potential EV owners.

63

This expanded charging network, along with EV-supportive municipal

codes for public and private parking facilities and workplace charging, is helping to drive

continued success. In addition, Tesla Motors has developed coast-to-coast fast charging for their

customers in the United States comprised of about 500 stations and nearly 3,000 chargers across

America and several in Canada, allowing cars to charge in minutes instead of hours.

64

The future

of EV charging research and development now lies in wireless power transfer—charging a car

without a power cord—which could open even more doors for future EVs in America.

As EVs have become mainstream, automakers are competing aggressively to design and deploy

the electric car of the future. With over 360,000 EVs deployed as of September 2015,

65

America

has one of the largest EV markets in the world and more and more Americans are abandoning the

gas pump and powering their cars with affordable, clean, and secure American energy.

63

Workplace Charging Challenge Newsletter: July 2015.

64

“Tesla Supercharger.” Accessed Aug. 21, 2015: http://www.teslamotors.com/supercharger.

65

Argonne National Laboratory, Light Duty Electric Drive Vehicles Monthly Sales Update, Accessed October 2015.

http://go.usa.gov/c3PeV

.

17

Revolution… Next

Our mission is innovation that continues to reduce the costs of a low carbon future from the near

term to the end of the century. The technologies highlighted in this report are already making a

big impact and are easily visible: wind towers dot the landscape, solar panels sprout on rooftops,

LEDs are on every hardware shelf, and the latest EV models can be seen on many neighborhood

streets.

Other emerging technologies that are not quite as visible will lead the next phase of the clean

energy revolution. In each case, deployment has begun to accelerate, costs have started falling,

and large-scale deployment could transform portions of the energy sector. The technologies

discussed here are among those to keep an eye on over the next five to 10 years.

18

Sweet Suite of Smart Building Technologies

A suite of new technologies will transform the way buildings use energy and interact with human

occupants. These “smart building” technologies may be easy to overlook, because they are

housed in familiar heating, ventilation, and air conditioning (HVAC) units and smart electricity

meters. However, their potential to increase the comfort of building occupants while saving

energy is immense. These devices can self-configure; communicate and self-diagnose

maintenance issues; learn building functions, floor plans, and layouts; and track occupancy

information to avoid complicated, expensive installation and maintenance scenarios and improve

user comfort. This feedback automates energy efficiency improvements and will help avoid the

need to crack a window when the office becomes too hot in the winter or bundle up when the air

conditioning is blasting in the summer.

Companies with large commercial facilities are starting to recognize the benefits of these

technologies and are working to retrofit existing heating and cooling units. These controls make

smart business sense with an average energy savings of 55% per unit, resulting in a one- to three-

year return on investment.

66

The potential for wider energy savings is also huge. Commercial

HVAC represents 250 billion kilowatt-hours of electricity use

67

and the addition of smart

controls to a subset of very large HVAC units less than 10 years old could lead to a savings of 37

billion kWh/year—more than the total amount of electricity generated in Nevada.

68

Smart meters on homes and businesses can enable energy savings and increase the flexibility of

the electricity grid. Advanced metering devices enable two-way communication between the

meter and the electricity provider and interface with smart thermostats and appliances (including

those large connected building HVAC units). Both allow utilities to better manage peak power

demand and assist the consumer in managing their own building energy use.

69

With 51.9 million

smart meters installed as of 2013, households and businesses are starting to take advantage of

this infrastructure and savings opportunities.

70

Key challenges to wider adoption of these technologies include the ability to install the product

directly out of the box, more easily install upgrades and perform maintenance, and enhancing

security. Smarter buildings will mean smarter energy use, which will lead to greenhouse gas

reductions, energy bill savings, and more comfortable homes and offices. It doesn’t take years of

schooling to see the time has come for this smart idea.

66

Wang, W.; et. al. Advanced Rooftop Control (ARC) Retrofit: Field-Test Results. Pacific Northwest National

Laboratory (PNNL), July 2013. http://go.usa.gov/3Sn3w

.

67

60% of cooling and ventilation load from: U.S Department of Energy, Buildings Energy Data Book, Table 3.1.4.

Accessed October 2015. http://buildingsdatabook.eren.doe.gov/

.

68

Internal U.S. Department of Energy Building Technologies Office calculations and

http://www.eia.gov/electricity/state/nevada/

.

69

Pratt, R.G., et. al. The Smart Grid: An Estimation of the Energy and CO2 Benefits. PNNL. January 2010.

http://go.usa.gov/3Snc5

.

70

U.S. Department of Energy, Energy Information Administration. Electric Power Annual 2013. “Table 10.10.

Advanced Metering County by Technology Type.” Accessed October 2015. http://go.usa.gov/3Snx4

.

19

Freight Trucks That Can Keep on Trucking

Tractor trailers, big rigs, semi-trucks, 18-wheelers—whatever you call them, these heavy trucks

are critical to economic activity, serving as the backbone of our domestic freight transport,

hauling nearly 73% of freight tonnage. Although freight trucks comprise only 4% of on-road

vehicles, they are responsible for almost 26% of U.S. on-road fuel consumption, representing a

huge potential for reducing the U.S. transportation sector’s energy and climate change impacts.

71

DOE’s Vehicle Technologies Office initiated the SuperTruck program in 2010 with the goal of

increasing the freight efficiency of long-haul trucks by 50% in 2015 compared to 2009. Four

teams were competitively selected for this five-year effort, and were led by Cummins/Peterbilt,

Daimler Trucks North America (DTNA), Navistar, and Volvo Trucks North America. These

manufacturers represent more than 90% of the U.S. market share for trucks. This program has

been a success with the top performing truck so far greatly exceeding the original goal, achieving

a 115% improvement in freight efficiency.

72

The technologies that enable these significant fuel efficiency improvements are actually a suite

of innovations that, in aggregate, result in big impacts. Modifications to the trailer that improve

aerodynamics and low rolling resistant tires can be easily paired with existing trucks to achieve

up to 27% fuel savings. One incredibly simple but effective example is the “skirts” that are now

often observed below the side and between the wheels of the trailer to reduce drag. Soon to be

released engines are expected to be at least 15% more efficient and will include advanced

powertrain electronics that will deliver gains in fuel economy through optimization and precise

control of combustion, fuel injection, air handling, and reductions in friction and other energy

losses.

With a combined DOE and industry investment of $270 million in developing SuperTruck

innovations, the technologies are already seeing commercial deployment or will be commercially

available in the near future. Overcoming the challenges that still remain in bringing some of the

more advanced solutions to market is a core goal of the Department’s follow on SuperTruck II

effort. Taken as a whole, SuperTruck technologies could achieve significant market penetration

in the near term and could result in a cumulative savings of nearly 290 million barrels of oil by

2020.

73

71

Federal Highway Administration, Highway Statistics 2013. “Table VM-1: Annual Vehicle Distance Traveled in

Miles and Related Data.” Accessed October 2015. http://go.usa.gov/3SnxP

.

72

U.S. Department of Energy, Vehicle Technologies Office. SuperTruck Team Achieves 115% Freight Efficiency

Improvement in Class 8 Long-Haul Truck. April 2015. http://go.usa.gov/3SnxG

.

73

U.S. Department of Energy. DOE SuperTruck Program Benefits Analysis. Prepared by TA Engineering.

December 2012. http://go.usa.gov/3SnC3

.

20

Vehicle Lightweighting: Lighten the Load and Hit the Road

Vehicle lightweighting is a key tool in developing the next generation of cars that achieve

significantly greater fuel economy and reductions in greenhouse gas emissions. This is an

effective method of saving both energy and fuel because a lighter vehicle requires less power to

accelerate. This allows the engine—a large source of mass in the car—to be downsized while

maintaining vehicle performance. For example, a 10% weight reduction can increase vehicle fuel

economy by 6% to 8% and for EVs lightweighting can increase how far the vehicle can travel on

battery power.

74

Lightweighting requires new materials to be developed to replace the conventional steel and

other heavy car components without compromising strength, performance, or safety. Some of

these new materials, such as high-strength steel and aluminum, are already in use, and advanced

material innovations such as composites made from polymer matrices, carbon fiber, and glass

fiber are working their way to market. New manufacturing processes have also been developed

to process these materials at scale. Many of these materials and manufacturing innovations were

proven through a recent lightweighting project supported by DOE, which culminated with the

demonstration of a 23.5% lighter 2013 Ford Fusion.

75

This demonstration used today’s materials

with unique manufacturing processes that previously had not been implemented at high volumes.

As a result, these innovations are ready for market entry.

Investment in this area is also growing: Ford announced that its 2016 line of F-150 trucks will

include aluminum parts that shed nearly 700 pounds compared to previous models. In addition,

vehicle components manufacturer Magna, as a result of a DOE-funded program, has built two

plants in the United States to produce special types of lightweight aluminum parts that are

otherwise impossible to manufacture domestically. Earlier this year DOE’s LPO announced a

conditional commitment for a $259 million loan to Alcoa, Inc. to support the expansion of an

existing manufacturing facility to produce advanced high-strength aluminum for automakers

such as Ford.

76

Other innovations like carbon fiber wheels, fiberglass coil springs, and

lightweight body panels are just beginning to be introduced into the luxury car segment. For

example BMW’s I3 EV has carbon fiber body and other manufacturers like Tesla, Mercedes

Benz, and Land Rover have aluminum body vehicles currently available in the market.

With industry, academia, and national labs, DOE continues to invest in reducing technical gaps

in lightweight structural materials (aluminum, magnesium, future generations of advanced high-

strength steel, and carbon fiber composites) and processes to accelerate their use to improve

efficiency in high volume vehicles. Continued investment will enable a huge potential savings in

this area. Projected innovations in lightweighting and advanced high efficiency engines deployed

in one quarter of the U.S. fleet could result in a savings of five billion gallons per year by 2030.

77

74

U.S. Department of Energy, Quadrennial Technology Review. 2011. p.39. http://go.usa.gov/3SnC9.

75

U.S. Department of Energy. Road to Fuel Savings: Ford, Magna Partnership Help Vehicles Shed the Pounds.

August 2014. http://go.usa.gov/3SnCA

.

76

U.S Department of Energy. Energy Department Offers Conditional Commitment to Alcoa to Support

Manufacturing of Aluminum for Automotive Sector. March 2015. http://go.usa.gov/3SnCJ

.

77

U.S. Department of Energy, Vehicle Technologies Office. Lightweight Materials for Cars and Trucks. Accessed

October 2015. http://go.usa.gov/3SnrB

.

21

Conclusion

The clean energy technologies highlighted here are transforming how our nation produces and

uses energy. While challenges and uncertainty exist for these technologies, it is clear that they

are not some far away opportunity, but are now a significant part of the energy landscape. We

can and should plan on using them to clean our air, reduce our reliance on unstable oil markets,

and help build an economy that is more competitive and more efficient, while reducing carbon

pollution.

There are even more technologies that are just on the horizon. These will increase the efficiency

of the vehicles we depend on for travel and move goods, and the systems we use to manufacture

new products and control our buildings. Although not as visible to the public eye, these

technologies are every bit as important to the future clean energy economy, holding the potential

for significant energy savings.

DOE will continue to encourage these innovations by providing support for R&D, consumer

education, and industry and stakeholder engagement. With continued progress in critical

renewable and energy-efficient technologies like these, we can look forward to a future of clean,

American-made energy.